CMS Is Ending the Risk Adjustment Arbitrage Era (Here's What That Means for Your Health Plan Deals)

The 2027 Advance Notice reshapes which vendors win and which need to reposition. Five signals to know before your next health plan buyer conversation.

Upward Growth provides health tech leaders with the playbooks and proof to transform complex markets into real growth. Each week, we deliver clear, practical strategies on positioning, messaging, and growth, so leaders can close enterprise deals and build repeatable momentum.

🤝 Work with Ryan on payor growth strategy: Contact me

🟦 Connect with the author, Ryan Peterson, on LinkedIn.

💡 Newsletter sponsorships are available: Learn More

🎁 Unlocked: This post includes the full deep dive

Most Tuesday articles start with a free section and then continue behind the paywall. Today’s post is left completely open so you can read the entire edition.

Paid subscribers get the full deep dive every week, plus playbooks, case breakdowns, and the ability to reply with their own questions.

Most health tech executives don’t read CMS regulatory documents. They have teams for that. But when those documents reshape how your buyers think about spending, priorities, and vendor relationships, you can’t afford to be the last one in the room to understand what changed.

The 2027 Advance Notice dropped January 26, 2026. The major headline is a near-zero rate increase: 0.09% versus roughly 5% last year. LinkedIn is full of stock charts and hot takes from brilliant industry veterans, but, to me, the near-zero rate isn’t the story.

The story is how CMS got there and what it signals about where Medicare Advantage economics are headed. Two risk adjustment reforms eat almost the entire growth rate, and one of them takes direct aim at a practice that’s been central to MA revenue strategy for years: chart reviews. CMS explicitly called out $7.5 billion in payments for diagnoses that appeared in chart reviews but had no corresponding medical encounter. Starting in 2027, those diagnoses won’t count toward risk scores.

The coding arbitrage that drove MA margins is being systematically unwound. That changes which health tech companies win, which need to reposition, and which face hard questions about their value prop.

This article breaks down the four signals that matter for your sales conversations and your positioning, plus a deeper look at where CMS is taking MA economics over the next few years. You'll walk away knowing what your buyers are reacting to, which solutions are advantaged or disadvantaged, and the specific questions to ask in your next health plan meeting.

Key Dates

Advance Notice published: January 26, 2026

Comments due: February 25, 2026

Final Rate Announcement: April 6, 2026

Applies to: Contract Year 2027

Who Wins and Who Loses

Before diving into the signals, here’s the framework. CMS is shifting MA economics away from coding sophistication and toward clinical value delivery. That creates clear winners and losers, and your current positioning likely falls into one of these two categories:

If your company sits on the left side, this article is a warning. If you sit on the right side, this article is about how to press your advantage. If you’re somewhere in the middle, the next 12 months will determine which side you land on.

The four signals that follow break down what’s actually in the Advance Notice and what it means for your sales conversations. Then we’ll look at where CMS is heading beyond 2027 and what that means for health tech strategy.

Signal 1: CMS Just Put a $7.5 Billion Target on Chart Reviews

Urgency: Immediate. If this affects your positioning, start reworking it now.

The near-zero rate increase comes down to two risk adjustment reforms that eat almost the entire effective growth rate:

Model recalibration (-3.32% with normalization). CMS updated the risk model to use 2023 diagnoses to predict 2024 expenditures, rather than 2018/2019 data. This narrows the gap between MA and FFS coding patterns by capturing more recent trends.

Excluding unlinked chart reviews (-1.53%). CMS will no longer count diagnoses from chart reviews or health risk assessments that aren’t tied to a medical encounter. The agency called out $7.5 billion in 2023 payments for exactly these diagnoses. One in six Medicare Advantage enrollees had diagnoses added from chart reviews that weren’t documented elsewhere, meaning plans were paid for conditions with no evidence of active treatment.

(It’s also worth noting that CMS also announced it will exclude diagnoses from audio-only services).

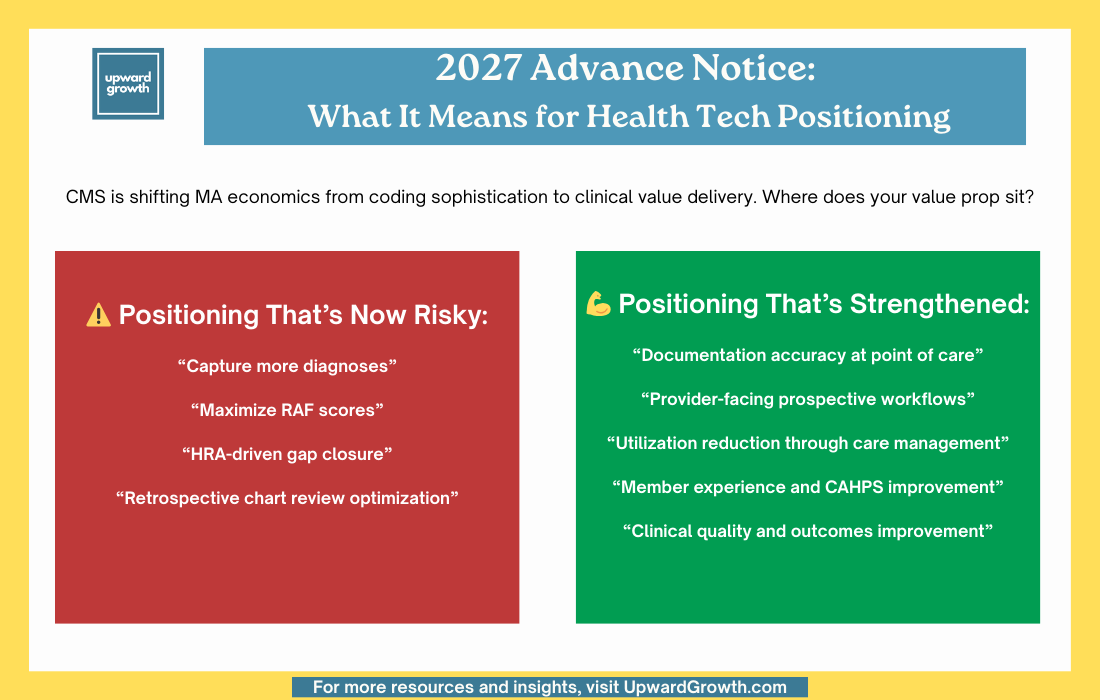

What this means for your sales motion: The language of “diagnosis capture” and “RAF optimization” now works against you. Plans that relied heavily on retrospective chart mining and HRA-driven coding got hit hardest in the stock market, as they had the most exposure to exactly what CMS is curtailing.

If your solution connects documentation to actual clinical encounters, your case just got stronger. Provider-facing workflows, prospective gap closure during care delivery, and clinical documentation integrity that improves accuracy rather than volume. That’s the winning positioning.

If your value prop was built around helping plans maximize risk scores through chart reviews, you have a positioning problem that needs to be solved quickly.

Question to ask buyers: “The unlinked chart review policy hits in 2027. How is your team rethinking documentation strategy, and where does that leave your current vendor relationships?”

Signal 2: CMS Is Leveling the Playing Field Between Nationals and Regionals

Urgency: Medium-term. Factor into account strategy and targeting over the next two quarters.

CMS laid out three principles guiding risk adjustment reform: simplicity, competition that works equally regardless of plan size, and payment accuracy. That second principle matters most for health tech vendors thinking about where to focus.

The “level the playing field for smaller, regional, and less well-resourced MA plans” language from the proposed rule is now showing up in actual rate policy. CMS is explicitly targeting the advantages that accrued to large nationals with sophisticated coding operations. The stated goal is that risk adjustment shouldn’t give larger, wealthier companies with more resources a competitive advantage.

Again, look at the stock market reactions. UnitedHealth and Humana got hit hardest as they had the most invested in the infrastructure that CMS is now devaluing.

What this means for your sales motion: If your customer mix skews toward large nationals, understand they’re facing both a rate hit and a structural shift away from their competitive advantages. Budget pressure will be real.

If you serve regional plans, take a clearer stance in your positioning. Regional plans often couldn’t compete as well in coding sophistication, which was a disadvantage (now it’s less of one). The gap is narrowing by design, and regionals may have more flexibility to invest in solutions that deliver genuine clinical value rather than scrambling to protect risk adjustment revenue.

This doesn’t mean national health plans stop buying; however, their buying criteria will most likely shift, and their budget scrutiny is intensifying. As such, regional and even smaller health plans may be relatively better positioned to invest.

Question to ask buyers: “With CMS explicitly targeting coding advantages that favored larger plans, how do you see your competitive position shifting over the next two years?”

Signal 3: Stars Measure Removals Shift Weight to Clinical and CAHPS

Urgency: 18 months. The measure removals hit 2028-2029 Star Ratings, but repositioning takes time. Start now.

The proposed rule’s removal of 12 measures is still on track. Operational and administrative measures are going away. Clinical outcomes, HEDIS measures, and CAHPS surveys gain relative weight.

The measures being cut are those on which everyone scored well, since they weren’t meaningfully differentiating plans. What remains will actually separate high performers from the pack. CMS has been explicit: the goal is to refocus the program on clinical care, outcomes, and patient experience where there’s meaningful variation across contracts.

There are two specific opportunities worth calling out here:

Depression Screening and Follow-Up is being added as a new measure (2027 measurement year, 2029 Stars). Mental health solutions now have a discrete, measurable hook tied directly to Star Ratings. If you sell anything in the behavioral health space, this is your talking point.

CAHPS and member experience measures gain relative weight as operational measures are dropped, thus making survey performance more critical. Solutions that improve member experience, reduce friction, and drive engagement scores gain ground as these measures carry more weight. And if you’ve been positioning around “member satisfaction” without a Stars connection, you now have one.

What this means for your sales motion: If your value prop ties to any of the 12 measures being removed, you have a limited repositioning window. The measures aren’t gone yet, but the smart money is already planning for a world without them.

Clinical quality improvement, gap closure, care management, behavioral health, and member experience are all relatively advantaged. If your pitch is "we help you hit operational Stars measures," it needs to evolve and fast.

Question to ask buyers: “The Stars measure removals shift weight toward clinical and survey measures. Which of those are you most concerned about, and where are you investing to close gaps?”

Signal 4: Part D Margin Pressure Is Permanent. Here’s Who Benefits.

Urgency: Ongoing. The IRA changes aren't new, but plans are still rebuilding their economics around them.

The IRA changes are now codified as permanent: a $2,000 out-of-pocket cap, elimination of the coverage gap, and increased plan liability in the catastrophic phase. The Part D risk model is also being updated to include reforms similar to those in Part C, such as excluding unlinked chart review diagnoses.

Health plans can't wait this out because the margin pressure is structural, not cyclical.

What this means for your sales motion: Pharmacy cost management, adherence, and MTM solutions continue to benefit from tailwinds. This isn't a temporary policy bump that might swing back the other direction. It's the new baseline.

The ROI case for anything that bends the Part D cost curve is cleaner than it’s ever been. Reduced pharmacy spend, improved adherence that prevents costly acute events, and specialty utilization management. All of these connect directly to a budget line that CFOs are actively trying to protect.

Question to ask buyers: “Part D margin pressure is locked in. Where are you seeing the biggest cost drivers, and what’s your priority for managing them in 2027?”

The Strategic Layer: Where CMS Is Taking MA Economics

Each signal above matters on its own, but the pattern across them tells you something bigger about where to place your bets.

V28 changed how diagnoses are weighted. The unlinked chart review exclusion changes how diagnoses are sourced. The Stars measure removals shift what plans get rated on. Each of these moves all point in the same direction: CMS is systematically unwinding the economics that rewarded coding sophistication and replacing them with economics that reward clinical value delivery.

If you're selling into MA, four strategic implications follow from this trajectory. These aren't about what to do this quarter. They're about where to position for the next three years.

1. The ROI conversation is shifting from revenue capture to cost reduction.

When coding arbitrage drove MA margins, plans could tolerate higher medical costs because those costs were offset by higher risk scores. However, as risk adjustment revenue compresses, the only path to margin protection is actually reducing the cost of care: care management, chronic condition management, transitions of care, avoidable ED visits, and preventable readmissions. If your value prop still centers on helping plans capture revenue they’re missing, you’re selling into a shrinking budget while the budget for medical cost reduction grows. The large nationals are currently distracted by rate pressure, margin compression, and benefit cuts, but they’re actively seeking vendors who can demonstrate documented cost avoidance.

2. Retrospective documentation strategies are losing their value.

The chart review crackdown isn’t just about unlinked diagnoses. It targets the entire retrospective chart review model. CMS is making the standard clear: if it didn't happen during a clinical encounter, it doesn't count. What plans need now is help with accurately documenting in real time, closing gaps during visits, and capturing clinical complexity as part of care delivery.

This is a problem for plans because retrospective chart review was operationally easier. You didn’t need to change provider workflows or integrate into the care delivery process. You just reviewed records after the fact. The vendors who built businesses around that model now need to pivot, and the plans who relied on them may need new partners.

What plans need now is help with accurately documenting in real time, closing gaps during visits, and capturing clinical complexity as part of care delivery. That’s harder to execute because it requires provider adoption (meaning strong, positive relationships with providers!), EHR integrations, and workflow changes. But it’s where the defensible revenue lives. The vendors who can make real-time documentation easier for providers have an opportunity that wasn’t as urgent as two years ago.

If it didn’t happen during a clinical encounter, it doesn’t count.

3. Member experience is becoming a margin protection strategy.

For years, plans confused lavish benefits with member loyalty. When rates forced benefit cuts over the past two years, many discovered they didn't have the brand affinity they assumed they did. Members left. The time for platitudes about member experience is over, and the real work begins. Plans that maintain strong experience while tightening benefits have a competitive advantage over those that can't. Solutions that reduce friction, improve communication, and drive proactive engagement connect directly to both Stars performance and member retention.

And to be clear: member engagement isn't the same as member experience. Sending reminders and closing gaps is necessary, but it's not what builds the kind of loyalty that keeps members from switching plans. Engagement is operational. Experience is emotional. Plans need both, but only one protects against churn when benefits get cut.

4. Compliance and documentation integrity are becoming procurement criteria.

Health plans have always cared about compliance, but the enforcement environment has shifted. In May 2025, CMS announced plans to audit all 550 eligible MA contracts annually and is working through a backlog of audits covering payment years 2018 through 2024.

With DOJ actively pursuing False Claims Act cases and clawbacks becoming a real line item, plans are asking harder questions about their vendors: Does your solution create documentation we can defend in an audit, or does it create exposure? Vendors who can demonstrate that their approach strengthens compliance posture rather than just capturing revenue have an advantage. Those still leading with "we help you capture more" will find themselves on the wrong side of procurement conversations.

Question to ask buyers: “Given where CMS is heading, what capabilities are you building for the next three years versus just solving for 2027?”

Final Thought

The throughline between the proposed rule and the Advance Notice is clear: the risk-adjustment arbitrage era is ending. CMS is closing the gap between Medicare Advantage and Fee-For-Service coding, deliberately and methodically. The advantages that built MA margins for years are being unwound.

What replaces that arbitrage? Actual clinical value. Care management that reduces utilization. Quality improvement that moves the clinical Stars measures. Member experience that drives retention and CAHPS. Documentation accuracy, not documentation volume.

If that’s what your company delivers, this is the moment to say it directly. Stop hedging. Stop leading with features. Lead with the outcome: we reduce costs through better care, not better coding.

If your company was built around the old economics (which many are), the next 12 months are a repositioning exercise. The longer you wait, the harder that conversation becomes with health plan prospects who are already hearing a different message from your competitors.

First things first: look at your pitch deck, your website, your sales scripts, etc. Find every instance of language that sounds like “capture,” “optimize,” “maximize RAF,” or “improve coding.” Ask yourself whether that language helps you or hurts you in the current environment. CMS just told you where they stand. Your positioning should make clear where you stand, too.

The frameworks in the weekly Upward Growth newsletter help health tech sales and marketing teams navigate payor conversations as the market continues to shift.

If your colleagues are in those conversations, they should be reading this too.

🎁 Gift Your Team a Paid Subscription.

💡 Pro tip: Many subscribers expense Upward Growth through their company’s professional development, training, or learning budget. Here’s a one-minute email template to get your manager to approve expensing your subscription.

Signal 4 is where this connects directly to the employer side. The same margin pressure pushing MA plans toward pharmacy cost management and adherence solutions is creating downstream effects for self-funded employers. As health plans tighten their Part D economics, PBMs adjust formulary strategy, rebate structures, and utilization management criteria across all books of business, not just Medicare. Employers often don’t realize that a CMS policy change affecting MA plans can shift the formulary their commercial members use within the same contract year. The structural pressure you’re describing doesn’t stay in Medicare. It flows through.

This one sparked a great discussion on LinkedIn. Would love to hear your take too. Here's the thread:

https://www.linkedin.com/posts/ryan-peterson-1a20866_medicareadvantage-healthtech-riskadjustment-activity-7424503356678868993-9dV7