You're Not Imagining the Health Plan Deal Slowdown

The buying sequence at health plans inverted in the last 18 months. Financial scrutiny that used to happen only at the end now happens at the start as well.

Upward Growth is a health plan market advisory firm. We work with health tech vendors, investors, provider organizations, and management consultancies to build go-to-market strategy around how health plans actually buy, operate, and make decisions. This weekly newsletter is where we share what we’re seeing in the market.

🤝 Work with Ryan on payor growth strategy: Contact me

🟦 Connect with the author, Ryan Peterson, on LinkedIn.

📰 Newsletter sponsorships are available: Learn More

The buying sequence at health plans has inverted in the last 18 months. Financial scrutiny used to be an end-of-cycle review. It now applies twice; once upfront through the operating leader before finance ever sees the deal, and again at the end through the formal finance review that’s always existed. Participants describe the same pattern from different sides of the market: a first call goes well for a vendor, and the operating leader is interested. A follow-up is scheduled, and then the cycle slows or stops in a way that doesn’t match the energy of the first conversation. Meanwhile, investors hear it on portfolio-company forecast calls. And consultants hear it from clients explaining why a previously active opportunity went quiet. The buying motion has changed structurally, and most of the work across the payor ecosystem is still being done against the way decisions had been made.

The change isn’t dramatic enough to make headlines, which is part of why this shift has been harder to read. There’s no announcement, no press release, no single quotable executive change at a single named plan. The clearest description comes from the consulting firms watching plans most closely. McKinsey’s work on rewiring payers for digital and AI describes payers moving away from siloed transformation programs and toward capabilities embedded inside the operating functions that run the business. That’s the inversion in a different language. The financial and regulatory pressures in healthcare for the last two years have reshaped how health plan operating leaders run their own evaluation processes, and the new sequence has consequences for everyone whose work depends on understanding how plans buy.

This article works through what changed, why it changed when it did, what it does to the buying motion day to day, and what it costs the people whose pursuit motions, pipeline forecasts, engagement scopes, and operating models are still built for the older sequence. The free portion lays out the analysis. The paid section gives you what to do with it.

Operations and Finance Run the Same Conversation Now

The structural change is simple to describe and easy to miss if you weren’t already watching for it. Operating leaders within plans have started running financial logic in their own evaluations before vendors are even advanced to finance review.

The VP who owns Stars used to be able to advance a vendor proposal on operating merit and let finance handle the financial defense at the end. The same VP today is constructing the financial defense as part of the operating evaluation, either by pulling finance into the conversation early or by building the model themselves from finance-supplied templates. The operating and financial decisions occur in parallel rather than in sequence.

The shift is evident across multiple lines of evidence, each pointing to the same underlying integration. Cost containment, modernization, AI deployment, and member experience aren’t being absorbed at plans as four separate workstreams. They’re running as one integrated effort, and integration on that scale isn’t possible while operations and finance keep their reviews separate. HealthEdge calls this year “the great rebalancing” in its 2026 annual payer report, with managing rising costs ranked the top priority for the second straight year, and 85 percent of executives reporting that compliance burden is directly cutting into margins.

Bain’s 2025 healthcare IT investment survey of 228 provider and payer technology leaders shows the same pattern in how plans are choosing technology. Total cost of ownership has become the dominant payer vendor selection criterion, alongside functionality and scalability. Total cost of ownership is finance language. It’s now the operating leader’s first selection criterion, not finance’s last filter.

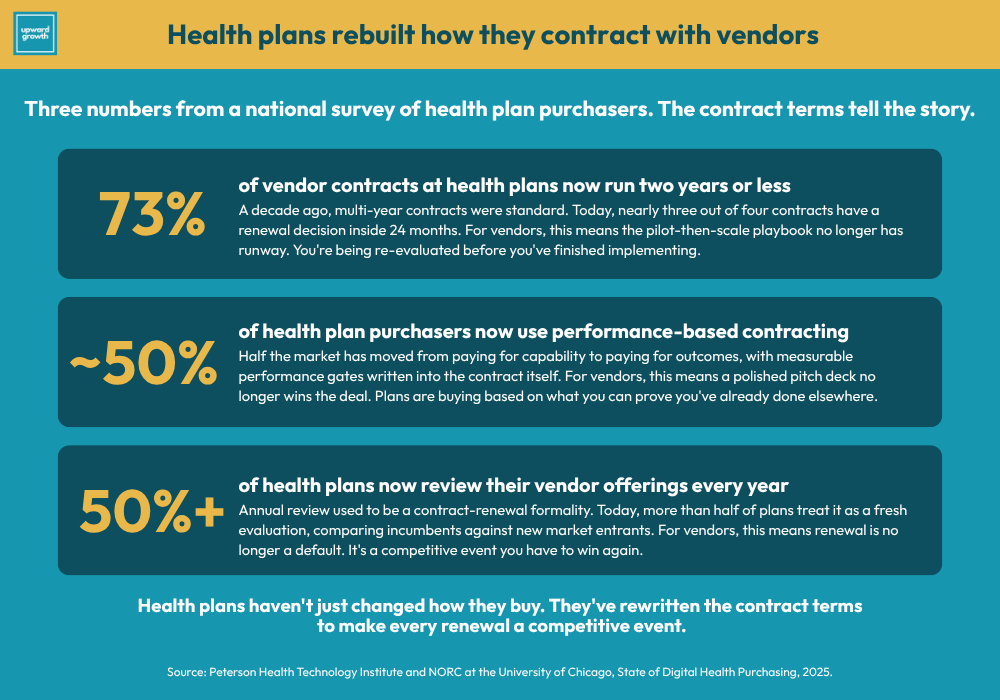

The contracting layer underneath the buying motion has been rebuilt around similar logic. Health plans are increasingly selecting vendors based on track record. In fact, performance-based contracting is in use by nearly half of purchasers and is growing. Seventy-three percent of vendor contracts run two years or less, and more than half of plans review their vendor solutions annually. The through-line is unmistakable: short contract terms with measurable performance gates are how plans run vendors when finance is in the room from the start.

This isn’t finance taking over operations, as operating leaders still own their metrics. But what has changed is what they are bringing to their own evaluations. They’re bringing finance with them, and they’re bringing it earlier than vendors are prepared for.

What Forced Operations and Finance to Integrate

Plans integrated operations and finance because the financial environment of the last two years made running them as separate conversations unaffordable. Five forces compounded across 2024-2026 to make integration the only response that worked.

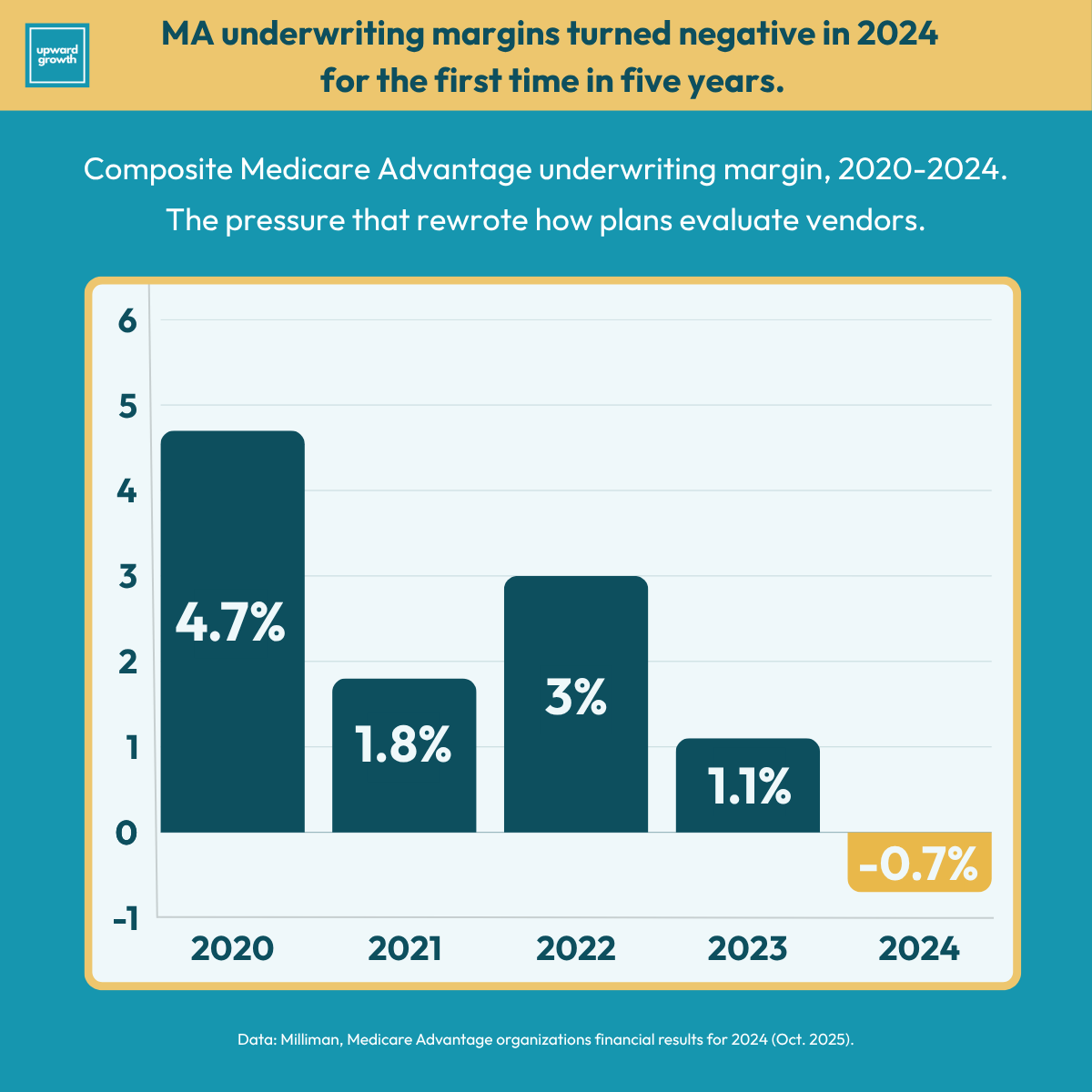

Margin compression at historic levels. Milliman’s analysis of 2024 statutory financial statements showed the composite Medicare Advantage underwriting margin at -0.7 percent for 2024, the lowest in five years. National carrier margins compressed about 20 percent year over year. The share of MA plans reporting positive underwriting margins fell from approximately 60 percent before 2020 to around 40 percent in 2023 and 2024. Every major MA carrier announced market exits, benefit cuts, or “margin over membership” pivots through 2025 and into 2026. At that level of pressure, every operating decision becomes a margin decision, which means the operating outcome and the financial defense have to be the same conversation.

V28 risk adjustment is fully phased in. V28 finished its three-year phase-in to 100 percent in payment year 2026, completing a methodology shift that consistently put downward pressure on average risk scores across the transition window. Plans absorbed that pressure by retraining clinical workflows, retooling HCC capture processes, and renegotiating provider arrangements. None of that work happens without finance in the room.

The CY 2027 risk model recalibration paused, not canceled. The CY 2027 advance notice proposed a further recalibration to a model built on 2023 diagnoses and 2024 expenditures. CMS subsequently paused it for the final rule, and the 2.48 percent rate bump in April 2026 came almost entirely from removing the recalibration from the math. The pause is a deferral, not a retreat. CMS has been explicit that the recalibration will return, and when it does, the math reverts to something closer to the 0.09 percent rate that landed in the January advance notice than the 2.48 percent in the April final rule. Plans pricing their next bid cycle, vendor commitments, and benefit design against the current rate are baking in a baseline they’re going to lose, and the operating leaders running those decisions know it, which is why finance is leading the next-cycle planning instead of reviewing it after the fact.

CMS-0057-F operational requirements live. The first public prior authorization metrics were due March 31, 2026, with API requirements taking effect in 2027. Compliance against operational SLAs is now visible publicly, which means the operating leaders who own those SLAs have to defend their technology investment choices against performance that their peers can see in real time.

Stars methodology rewriting toward member experience. CAHPS and HOS measures are projected to reach a combined weight in the high-30s percent of overall Star ratings by the 2029 measurement cycle. The shift moves Stars revenue away from operational compliance and toward measurable member outcomes, which changes which vendor categories actually move the bonus and changes how operating leaders defend Stars investment to finance.

Each force carries its own compliance cost, operating implications, and technology investment. Plans running them as five separate workstreams pay five separate coordination costs and produce five separate financial defenses for capital coming out of the same constrained budget. Integration is the response that makes the math work.

The plans furthest along this path didn’t announce the change. They started running their operating reviews differently.

Three Things This Changes About How Plans Buy

The integration changes the buying motion in three concrete ways. None of them are messaging refreshes. All three are structural.

1. Financial logic is now table stakes for the first conversation.

The operating leader doesn’t have time to advance a proposal that can’t withstand the financial defense they know finance will apply. They’re also not going to do that work for the vendor. A vendor that shows up to a first call with capability framing and ROI promises but no financial architecture (no model of which budget line is affected, no quantified outcome at the buyer’s plan size, no break-even analysis at lower performance, no answer to what happens if MLR runs high) is signaling that the buyer’s organization will have to do the financial construction itself. Most operating leaders won’t take that on.

The vendors winning at this level show up to first calls with the financial defense already built. I wrote about the specific questions CFOs ask when evaluating proposals (and how vendors can build materials that preempt them) last fall. The principles in that piece have only become more critical as operating leaders have started running those questions themselves, in the first conversation, before finance ever sees the deal.

2. Procurement, security, and (often) legal review now run alongside the operating evaluation, not after it.

In the older sequence, security questionnaires, BAA review, data use agreements, and procurement contracts were completed after the operating leader endorsed the deal. More frequently, they run in parallel much earlier in the process.

A vendor whose security questionnaire takes three weeks to complete, whose BAA template needs legal review, or whose data use agreement requires custom drafting is paying that time cost during the active operating evaluation rather than after. The vendors who move fastest hand over the entire package in the email after the qualification call, which signals seriousness in a way the operating buyer can read.

3. Track record now outweighs capability differentiation.

The recent PHTI data is direct on this. Health plans largely select vendors based on their track record, and the contracting environment rewards measurable performance and shorter contract lengths.

The vendors who can produce dated, attributed, plan-specific case studies covering financial outcomes (not just clinical or operational ones) are evaluated differently than vendors whose case studies live at the capability or pilot level. The pilot-then-scale market-entry approach that worked in the 2010s doesn’t work the same way now. Operating buyers under financial scrutiny aren’t running pilots without a clear path to enterprise scale.

The three shifts compound. A vendor without financial architecture loses the first conversation. Without parallel-track procurement-readiness, they lose the next two months. Without referenceable financial outcomes at comparable plans, they lose the comparison to the incumbent. The deals that used to advance through the gates one at a time now have to clear all three at once.

The vendors winning at this level show up to first calls with the financial defense already built.

What's Breaking in Pipelines, Diligence, and Engagements Right Now

The integration of operations and finance inside plans changes what's true about the buyer, which changes what's true about the work being done against that buyer. The four inputs most exposed are vendor pipelines, portfolio diligence, consulting engagement scopes, and a plan's view of itself. Each one is being valued today on inputs that have already changed underneath it.

Vendor pipelines are the most immediately exposed. A list of named opportunities at named operating leaders looks healthy on a forecast review, but the financial defense the deal will actually face is now the gating factor, and most pipeline reviews don’t surface it. Reps who can articulate how their proposal will hold up against the questions the operating champion’s CFO will ask have forecast quality. Reps who can’t are reporting confidence on opportunities that will die at finance, and the gap between projected pipeline and closed revenue is going to keep widening until the qualification standard catches up.

Portfolio diligence runs into the same blind spot one level up. Reviews of named accounts at portfolio companies typically check the buyer’s title, the rep’s relationship strength, and the deal stage. The new sequence requires a fourth check: whether the rep can construct the financial defense the deal will face. That answer doesn’t surface in a standard sales review and can usually be reconstructed in a focused conversation with the head of sales and the head of finance. Forecast risk is materially different across plans further along the integration versus plans still running the older sequence, which is a diligence question most frameworks haven’t started asking.

Consulting engagement scoping carries similar exposure. Payor strategy work scoped around clinical operations, vendor consolidation, or operating model design without explicit business case architecture is missing the financial layer plans now expect to see embedded in the work itself. Oliver Wyman’s TOMORROWPlan operating model work describes decision rights moving closer to the leaders who own the operating metrics, which means engagements designed for an older decision-rights map are landing in front of stakeholders with different priorities than the ones the work was scoped to serve. The scope that worked in 2023 is now a partial scope, and the engagements being won today bake CFO-defensible business case modeling into the deliverables rather than treating it as a separate workstream.

Health plan executives face a version of the same question internally. The integration has already started at most plans because the financial environment forced the issue. What's still being decided is whether it was deliberately designed or arrived as a series of late CFO vetoes. The first version produces an operating advantage, while the second produces the slowdown vendors are feeling at the front of every deal.

The four exposures compound. Pipelines built for the older sequence overstate forecast quality. Diligence reviews built for the older sequence miss the gating factor. Engagements scoped for the older sequence land in front of the wrong stakeholders. Plans that drift into integration rather than design the integration produce the slowdown their vendors are feeling. Whoever rebuilds their pursuit motion, diligence framework, or engagement scope against the new sequence first has the advantage.

Everything above is the analysis. Below is what I actually use with clients: a one-page champion brief that arms your operating champion for their CFO meeting, and the discovery language to use in the conversations you're already having.

Paid subscribers get this section plus the full archive of frameworks, scripts, and deep dives.

🔒 Upgrade to a paid subscription to keep reading.