An Actuary Is About to Run Cigna. The Pattern of Moves Already Tells You What He Thinks.

Three divestitures in eighteen months and what comes next.

Upward Growth provides health tech leaders with the playbooks and proof to transform complex markets into real growth. Each week, we deliver clear, practical strategies on positioning, messaging, and growth, so leaders can close enterprise deals and build repeatable momentum.

🤝 Work with Ryan on payor growth strategy: Contact me

🟦 Connect with the author, Ryan Peterson, on LinkedIn.

📰 Newsletter sponsorships are available: Learn More

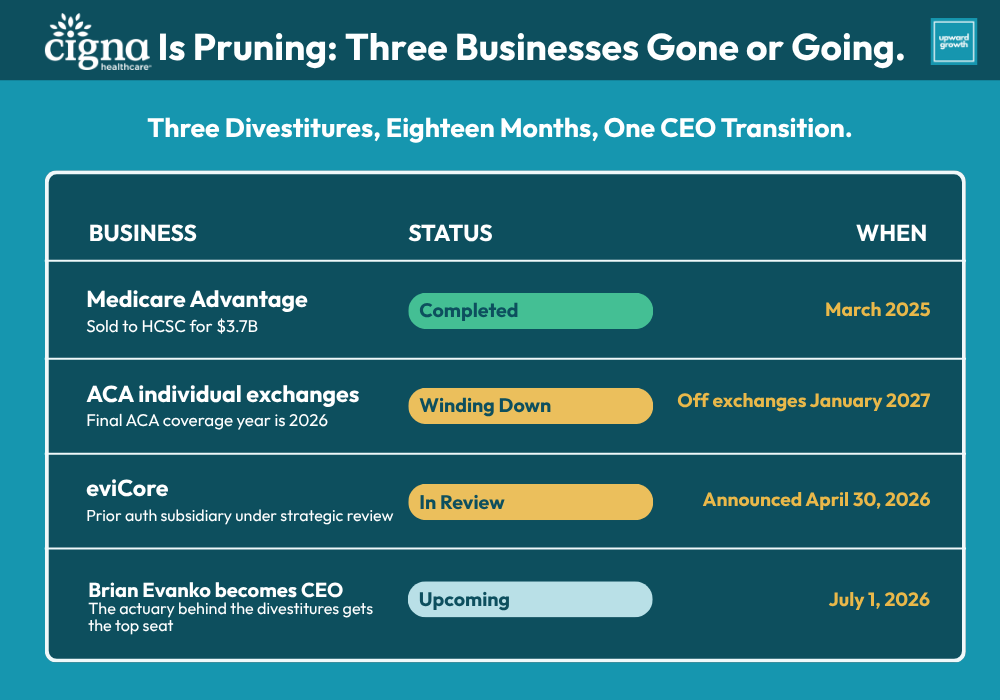

Brian Evanko, the incoming CEO of The Cigna Group, used the phrase “portfolio shaping” twice on the April 30 earnings call. Once to describe the Affordable Care Act (ACA) individual exchange exit and once to describe the eviCore strategic review. Two announcements presented as a single coordinated decision, both “proactive” and “based on a deliberate review of management focus, relative size and scale, as well as the degree of standardization and automation.” That’s the language of a CEO who’s been running the numbers for two years and finally has authority to act on them.

Add the Medicare Advantage book Cigna sold to Health Care Service Corporation (HCSC) for $3.7 billion in March 2025, announced fifteen months before that. Three businesses divested, exited, or are in active strategic review within eighteen months. Cigna posted $1.7 billion of net income on $68.5 billion of revenue, raised 2026 guidance, and used the same call to walk away from two more lines of business. The earnings beat got the press treatment. The repositioning is the story.

Evanko becomes CEO on July 1. He’s an actuary through and through. Fellow of the Society of Actuaries (FSA), Member of the American Academy of Actuaries (MAAA), Chartered Financial Analyst (CFA). He spent the bulk of his Cigna career as CFO before taking operating roles. From 2017 to 2021, he personally ran Cigna Healthcare’s U.S. Government business. Medicare Advantage. Medicaid. Individual and Family Plans (IFP). Every book Cigna is now exiting.

The April 30 earnings call was his opening statement as the incoming CEO. The portfolio shaping language was his. So were the ACA exit and eviCore review decisions. If you sell to payers, partner with them, invest in them, advise them, or compete with them, the read-through is sharper than the headlines suggest. The Cigna account you knew at the start of 2024 is already gone. By 2027, it won’t be recognizable.

The Profile Behind the Pattern

David Cordani spent seventeen years as CEO and grew Cigna from an $18 billion regional insurer into a $275 billion integrated health services company. The Express Scripts acquisition closed in 2018. The Evernorth rebrand unified the services and supply businesses in 2020. Total shareholder return ran north of 750%. Diversification was the strategy, and it worked.

Evanko’s profile is different. He served as CFO before running the U.S. Government business from 2017 to 2021, then returned to the CFO role. In January 2024, he was named President and CEO of Cigna Healthcare. In March 2024, he became President and Chief Operating Officer of the entire Cigna Group. In 2025, he took unified responsibility for both Cigna Healthcare and Evernorth. On March 3, 2026, he was named the CEO's successor. Each step concentrated decision authority on the person who already had the deepest read on Cigna’s capital base, member economics, and segment-level returns.

What Evanko said on the call shows how he thinks.

He framed the ACA exit two ways. The team did not see the potential to scale the marketplace business to make a significant impact in the broader enterprise. The blunter version: “This is small business for us today, and it’s been shrinking in recent years.” The reason was relative size, not cost trend. Cigna’s first-quarter ACA margins improved alongside the rest of the industry as carriers repriced for 2026. The exit was about relevance, not margin. The line was too small to earn the capital and management attention it required.

The eviCore framing was sharper. Evanko said industry progress toward standardizing and automating prior authorization could open new doors for the eviCore business, potentially leading to a partnership or combination with our complementary industry participants. That’s a CEO previewing the buyer pool while announcing the strategic review. The framework is settled. What remains is execution.

Cigna’s incoming CEO ran Cigna’s Government books from 2017 to 2021. He’s the one moving Cigna out of those books now. The moves carry his signature.

The next two years won’t be quiet. Evanko’s framing on the call (”management focus, relative size and scale, as well as the degree of standardization and automation”) is a four-variable test for any line of business. Run it against any Cigna segment and you can sketch the answer he’ll reach in 2027. Lines earning their capital and management bandwidth get more of both. The lines that don’t earn their keep get strategic alternatives or divestitures.

The lens has changed. Cordani built. Evanko prunes. Both are coherent strategies. They produce different companies and different relationships with everyone selling into them.

Cigna’s incoming CEO ran Cigna’s Government books from 2017 to 2021. He’s the one moving Cigna out of those books now. The moves carry his signature.

When the Board Promotes the CFO

The Evanko archetype isn’t new. Boards have a history of promoting finance executives into the CEO seat at scaled payers when the diversification phase has run its course and the next chapter requires sharper capital allocation. The closest recent precedent is Joe Zubretsky at Molina.

Zubretsky took over Molina Healthcare in November 2017. Former Aetna CFO, former CEO of Hanover Insurance, and finance executive in the same mold as Evanko. He inherited a company that had just posted a $512 million loss and an executive shake-up. His first eighteen months produced a textbook portfolio rationalization. Molina Medicaid Solutions was sold in Q3 2018, and high-cost provider contracts were terminated or renegotiated, networks narrowed, and stop-loss thresholds reset. Non-strategic health plans were evaluated for exit. By the end of 2018 Molina’s net income had swung from a $512 million loss to a $707 million profit, the company had repaid more than $750 million in debt, and the divestiture cycle was largely complete. The pattern was concentration where the segment was performing, exit where it wasn’t, and a hard look at every contract structure that touched margin.

Wayne DeVeydt is the broader version of the same pattern. Anthem CFO from 2007 to 2016. Then CEO of Surgery Partners, then operating partner at Bain Capital, now CFO of UnitedHealth Group as of September 2025. Finance-first executives keep getting pulled back into operating roles at scaled payers, even as boards want margin discipline and portfolio focus. That’s not coincidence. It’s the move boards make when the integration and growth chapter has produced the company it was going to produce, and the next chapter needs sharper capital allocation than the prior CEO was built for.

The Cordani-to-Evanko transition fits the same archetype. The build phase produced a $275 billion company. The next phase requires deciding which lines of business inside that company deserve the capital and management attention they’re consuming. That decision-making belongs to a CFO's mind. The Molina case is the cleanest recent precedent for what the playbook looks like in motion. The divestiture cycle was largely complete within eighteen months of Zubretsky's arrival. Cigna is roughly fifteen months in from Evanko taking unified responsibility for Cigna Healthcare and Evernorth in 2025. The April 30 announcements land right on the timeline a Zubretsky-style portfolio rationalization would predict. Whether the next eighteen months produce a similar pace of further moves is the open question (but precedent says yes).

The Earnings Call vs the Coverage

Two readings of the April 30 announcements have circulated this week in payer-facing trade press, vendor sales decks, and PE memos. Each captures part of the picture, and each looks different next to what Evanko actually said.

The first is that this is an ACA cost-trend story, with Cigna following Aetna out of an unsustainable category. Premiums up, enrollment down, subsidies expiring, margins compressing. That’s the backdrop. The trigger was different. Cigna’s Q1 ACA margins improved alongside the rest of the industry. Evanko’s stated reason was different: “small business for us today, and it’s been shrinking in recent years.” The exit was driven by relative size.

The second is that the eviCore review is being driven by regulatory pressure on prior authorization. Federal and state prior authorization (PA) reforms have intensified, and the easy story is that Cigna is divesting a politically exposed asset. Evanko’s framing inverts that. He cited industry-standardization and automation as reasons eviCore could be more valuable outside Cigna than within it. The pitch was framed as upside-down, with the strategic review as a sales process with the buyer pool already in mind.

How Cigna Will Buy Differently in 2026 and 2027

Three buying behavior shifts are already in motion.

Cigna’s procurement focus is concentrating on commercial retention and specialty cost economics. On the call, Evanko said he intends to position Cigna as “the clear leader in consumer-focused and AI-enabled health services, with an emphasis on clinically complex patients.” That’s a buyer who spends on broker enablement, employer-direct partnerships, ASO retention tools, behavioral health integration, network design flexibility, and specialty cost trend management. With MA gone to HCSC over a year ago and ACA winding down through 2026, the Government program buyer at Cigna is functionally retired. If your product roadmap was built around that buyer, you need a different home plan.

The Signature pharmacy model is now a forcing function across every vendor relationship that touches Evernorth. Cigna is targeting a rebate-free pharmacy structure with roughly 30% lower brand pricing and 50% adoption by 2028. That changes how Express Scripts evaluates partnerships, how Accredo structures specialty contracts, and how MDLive prioritizes clinical integration. A vendor aligned with the rebate-free model has traction available in 2026. A vendor whose economics depend on rebate flows is looking at either 2 years of value proposition rebuilding or shrinking renewals.

Given that eviCore is now likely to be shopped, expect a 6 to 12-month procurement freeze on workflows it touches. And anyone selling into eviCore-managed utilization management (UM) and PA workflows at Cigna should run two parallel scenarios. One where eviCore lands with a strategic acquirer holding adjacent UM assets, and one where it lands with a private equity (PE) sponsor running it for cash flow. The buyer profiles produce different procurement behaviors, technology priorities, and contract structures.

The three shifts add up to a Cigna that's sorting its segments into three different procurement states at once. Vendors with an active 2026 Cigna conversation know which state each of their relationships is in.

How Cigna Will Partner Differently

Buying behavior is one signal. Partnership structure is the other, and it tends to lag the buying signal by a quarter or two before the shifts become visible.

Cordani-era Cigna was structured to do big, multi-year strategic partnerships across business units. The Express Scripts integration is the obvious example, but the same pattern appeared in smaller deals as well. Point solution vendors signed strategic alliances that simultaneously touched Cigna Healthcare and Evernorth, with commercial and specialty teams co-selling and partnership economics that assumed cross-business-unit value capture. The diversification thesis required that kind of partnership architecture, and Cordani's team built it.

The first thing to watch is what happens to the existing Cordani-era strategic alliances. Some of those partnerships are safe under Evanko’s framework because the partners are embedded in lines of business that are receiving more capital, including specialty pharmacy partnerships through Accredo, employer engagement partners that drive ASO retention, and platform partners supporting the Signature pharmacy build-out.

Others don’t sit as comfortably. Strategic alliances built around cross-business-unit value, where one of the business units is now winding down or under review, will get the same four-variable test Evanko is applying to the lines of business themselves. If the partnership doesn’t pass on its own merits inside Commercial or Evernorth or Express Scripts, the renewal conversation gets harder. Vendors and partners currently inside Cordani-era alliances should expect those agreements to be reviewed in light of the new framework, and should know which side of the line their partnership lands on before the renewal conversation opens.

Four forward shifts to expect on new partnerships:

PBM-led co-selling becomes more central. Cigna’s center of gravity has shifted toward Evernorth and Express Scripts, and the Signature rebate-free pharmacy model is the strategic bet that has to work. Vendors whose economics align with Signature, whose data integrates cleanly with Express Scripts, or whose specialty pharmacy story plugs into Accredo will find Evernorth willing to co-sell into employer accounts in ways that didn’t exist in 2024. The opportunity is real, and so is the cost. Co-selling arrangements with PBMs typically include rate concessions, exclusivity provisions, or revenue share commitments. Vendors entering those conversations need a position on what they’re willing to give up for the distribution.

AI and data partnerships get evaluated differently than they did a year ago. Evanko’s positioning of Cigna as the leader in “AI-enabled health services” isn’t generic earnings call language. It signals that AI and data partnerships are now strategic infrastructure rather than experimental pilots, which changes the procurement bar. Pilots that produced inconclusive ROI in 2024 don’t get renewed. Partnerships that demonstrated measurable trend impact, claims accuracy improvement, or specialty cost reduction get expanded. Vendors with AI capabilities that map to Evernorth’s specialty cost mandate or Express Scripts’ Signature build-out will find Cigna a more aggressive partner in 2026. Vendors whose AI doesn’t tie to a specific line-of-business outcome will find the partnership conversation has grown more skeptical, even when the underlying technology is strong.

Employer-direct partnerships become a competitive lane. Commercial and ASO are now the primary buying centers at Cigna Healthcare, which puts pressure on Cigna to differentiate on employer experience, broker support, and specialty cost outcomes. Vendors with employer-direct distribution are more interesting partners than they were when Cigna was simultaneously optimizing across MA and ACA. The flip side is that Cigna will also pursue employer-direct deals aggressively itself, which means the same vendor capabilities that make a partnership attractive can look like a competitive threat. Read the partnership conversation in that light.

Cross-business-unit deals get harder to close. When the businesses themselves are being evaluated for relative scale and management focus, cross-business-unit partnership economics become a tougher pitch at the executive level. A vendor pitching a deal that requires alignment between Cigna Healthcare and Evernorth now has to make the case to two separate buying tables, with two separate procurement teams running their own versions of the four-variable test to determine whether the partnership is worth the management attention. Deals that would have closed as a single Cordani-era strategic alliance now look more like two parallel single-line-of-business deals.

The structural takeaway is that partnerships with Cigna over the next two years will be smaller, more focused, and more transactional than the Cordani-era strategic alliances. The environment is different, not worse. The vendors and partners who recognize the shift early will be positioned for the deals that close.

Finally, for investors with payer-services portfolio companies (portcos), the same logic surfaces two beats at the fund level. eviCore's potential market entry at scale resets the comp set for UM and PA assets. Whoever buys it (a strategic with adjacent UM assets, a PE platform building a vertical, or a recapitalized standalone) becomes a meaningful comp for any UM-adjacent portco, and that comp will set or compress multiples across the category. Portfolio theses built around "diversified national payer exposure" also just got narrower. The peer set fragmented into five companies doing five different things, and limited partners (LPs) will ask sharper questions about which specific payers and lines a thesis depends on. The defensible answer in 2026 is line-of-business-specific. Category-level theses are gone.

The Pattern Across the Other National Health Plans

There’s a useful parallel from one year back. CVS Health announced Aetna’s ACA exit on May 1, 2025, affecting roughly one million members across seventeen states. Cigna’s announcement came April 30, 2026. One year apart almost to the day. Two of the largest national payers reached the same conclusion on the same line of business inside twelve months.

The pattern question for the rest of the national plans writes itself. UnitedHealth, Elevance, and Humana each face their own version of the focus-or-divest math, and the Q1 calls already hinted at how those decisions are being made. That’s the subject of next week’s piece in this newsletter, where we’ll walk through what the Q1 cycle has already said and where the Q2 and Q3 calls are most worth tracking. The week after that, we’ll look at what the post-Aetna and post-Cigna ACA picture means for the underlying health of the marketplace itself. That’s a different conversation from the leadership-driven repositioning Cigna’s call surfaced.

The diversified national payer label was always more of a Wall Street comp set than an operating reality, and Cigna fit it least of the five. UnitedHealth has Optum and the provider assets that come with it. Elevance has regional Blues geography. Humana is now a pure-play MA. Cigna built into a pharmacy and specialty company with a commercial insurance arm, and the April 30 announcements made the operating reality match what the segment economics already showed. The Blues' consolidation of the last two years told a parallel story in a different geography. The “national plan” comp set is already collapsing into five companies that do five different things.

For anyone selling into payers, the addressable plan list for any given product is getting smaller and sharper. Total Addressable Market (TAM) work that assumed access to all national plans as the buying universe is now outdated, and the peer group has fragmented faster than most comp models have been updated. That gap is the operational risk on every payer-facing pipeline right now.

Final Thought

The April 30 announcements sit on top of a Medicare Advantage divestiture that closed last March and a leadership transition that names Evanko CEO July 1. The framework Evanko described on the call (management focus, relative size and scale, standardization, automation) is now in the public record, and the divestitures that match it are underway. Account plans built on the 2024 version of Cigna are stale. Comp models that still group Cigna with the diversified nationals are using a category that’s been a Wall Street fiction for two years. Vendors and investors who see the April 30 announcements as the start of an eighteen-month repositioning will hear the next two earnings cycles differently than those who see them as one quarter’s news.

What’s still being written is whether the rest of the national plans run a version of the same calculation, and how soon. Q2 and Q3 calls at Elevance, UnitedHealth, and Humana are now must-listen events. Cigna moved first among the post-Cordani-era nationals. Whether anyone moves next, and how soon, is the open question for the rest of 2026.

The weekly Upward Growth newsletter gives health tech vendors, investors, provider organizations, and management consultancies a clearer view of how the payor market actually works.

If your colleagues are making decisions in this market, they should be reading this too.

💰 Invest in your team with a paid subscription.

💡 Pro tip: Many subscribers expense Upward Growth through their company’s professional development, training, or learning budget. Here’s a one-minute email template to get your manager to approve expensing your subscription.