Five Health Plan Postures to Understand During the 2026 ACA Shakeout

Aetna and Cigna walked. Subsidies expired. Every plan staying in is making a different bet on what the market becomes.

Upward Growth provides health tech leaders with the playbooks and proof to transform complex markets into real growth. Each week, we deliver clear, practical strategies on positioning, messaging, and growth, so leaders can close enterprise deals and build repeatable momentum.

🤝 Work with Ryan on payor growth strategy: Contact me

🟦 Connect with the author, Ryan Peterson, on LinkedIn.

📰 Newsletter sponsorships are available: Learn More

In 2017, I was selling into health plans when UnitedHealth, Aetna, and Humana walked away from the Affordable Care Act (ACA) exchanges. The execs I'd been working with at midsize plans (the people who decided which vendors and partners got funded) went radio silent for months while their leadership figured out whether to follow. Even procurement teams paused ACA-adjacent deals that we were in the process of contracting, since everything was up in the air. Two years of relationship-building went on hold while plans worked out their 2018 posture.

That’s the lens I keep coming back to as I try to interpret 2026, as the ACA is shuffling itself again. Aetna walked in 2025. Cigna walked in 2026. Baylor Scott & White Health Plan, Providence Health Plan, Molina at the service area level, and a cohort of regional plans have all announced retreats of varying depth. Enhanced premium tax credits (ePTCs) expired at the end of 2025. Bronze plan migration is reshaping the risk pool in real time. A Republican Congress is heading into midterms with no replacement plan after 15 years. The plans staying in are taking five distinct strategic postures, and reading those postures (rather than reading the headlines) is how to make decisions about this market in 2026 and 2027.

One trap to avoid before the comparative work begins. The convenient story is that 2017 was a narrow exit (the three commercial nationals) and 2026 is a broad multi-tier retreat. That framing is wrong. The 2017 shakeout was just as broad, possibly broader by raw insurer count. What’s genuinely different about 2026 is the cause, the mechanism, and, in Molina’s case, the scale of a single operator’s pullback. Misreading 2017 leads to misreading what comes next.

The 2017 Shakeout Was Broader Than You Remember

Back in 2017, the headline story was that UnitedHealth, Aetna, and Humana walked. The actual story was broader. In fact, Becker’s Payer Issues documented 48 insurers that reduced their 2017 ACA exchange footprint. Every plan category currently making news in 2026 had an analog in 2017. Commercial nationals walked at scale (UnitedHealth across 28-plus states, Aetna across 11). Medicaid-DNA operators pulled back from individual markets, too. Provider-sponsored plans exited in numbers that should look familiar to anyone reading the 2026 retreat (more than a dozen health-system plans contracted or exited that year, including Scott & White Health Plan, the predecessor plan in the same Baylor Scott & White Health family, announcing its 2026 exit recently). State Blues retrenched in PPO and county footprints. Even tech-native plans were sorting themselves: Oscar exited New Jersey and Dallas in 2017 (the same Oscar that’s now profitable and growing).

The story underneath the plan-level retreat was the collapse of the ACA co-ops, with 17 of 23 closed by mid-2017 and hundreds of thousands of members displaced. The co-op story is critical because it’s the closest 2017 analog to what’s happening to Medicaid-DNA operators like Molina now: a category of plan designed for this market that still couldn’t make the operating math work at the scale required. The aggregate effect was that the average number of insurers per state dropped from 5.6 in 2016 to 4.3 in 2017, then bottomed at 3.5 in 2018. Single-insurer counties went from 7% to 31% in a single year. The dominant narrative at the time was “death spiral.”

What actually happened was a shakeout that sorted across every category of operator. Centene leaned in through Ambetter even as it pulled out of Wisconsin. Some Blues absorbed displaced membership while others retrenched. Medicaid-DNA operators consolidated where the underwriting worked. Enhanced premium tax credits arrived in 2021 under the American Rescue Plan, and enrollment grew to 24.3 million by 2025. The plans that emerged stronger weren’t the ones in a particular category. They were the ones whose operating models fit a smaller, sicker, more price-sensitive pool.

What’s Genuinely Different in 2026: Four Contrasts, One Cause Profile

Aetna walked again in May 2025. Cigna walked in April 2026. Both decisions landed almost exactly one year apart. Premiums are up roughly 26% on average. Net enrollment dropped from 24.3 million to 23.1 million. Bronze plan share jumped from 30% to 40% in a single year. The retreat extends beyond the nationals into provider-sponsored plans, Medicaid-DNA operators, and regional plans, as it did in 2017.

Four things actually distinguish 2026 from 2017, and they roll up to a single observation about cause: the 2017 shakeout was driven by initial-market actuarial losses on a still-maturing risk pool and by the co-op funding shortfall when risk corridor payments never materialized. That said, the 2026 shakeout is largely driven by the ePTC cliff and capital allocation pressures within vertically integrated insurers. Both forces genuinely did not exist as primary drivers in 2017, and the four differences below show how those two new primary drivers are emerging in the operating environment.

1. Subsidy environment. 2017 happened with the ACA’s original subsidy structure intact. 2026 is happening after the enhanced premium tax credits expired and were not renewed. KFF estimates subsidized enrollees’ average net premiums rose 114%. The pricing pressure on enrollees is operating in real time.

2. Bronze plan migration. A 10-percentage-point shift in plan tier mix in a single year is among the largest single-year tier shifts in marketplace history. The 2017 shakeout reshaped which plans were in the market, but the 2026 shakeout is reshaping which products inside the market are growing and shrinking.

3. Vertical integration math. The three largest national payers now sit under parent companies with major non-insurance businesses: UnitedHealth and Optum; CVS Health and Aetna; and Cigna and Evernorth/Express Scripts. Aetna's 2017 exit was driven by actuarial losses. Aetna's 2025 exit and Cigna's 2026 exit are capital allocation decisions evaluated against adjacent businesses that can absorb the capital and management bandwidth an ACA presence consumes. That contrast is structural and didn't exist in 2017.

4. Tech-native maturity. In 2017, Oscar exited New Jersey and Dallas while still figuring out the model. In 2026, Oscar is profitable, growing, and operating with a disciplined posture. Bright Health collapsed in 2023, and the takeaway (capital discipline matters more than growth velocity) shaped how every surviving tech-native plan operates today.

The political environment is the connective tissue underneath those four contrasts rather than a separate one. The Republican Congress chose not to extend the ePTCs before they expired at the end of 2025. The Trump administration's regulatory and reconciliation actions, including the One Big Beautiful Bill Act (OBBBA) Medicaid cuts and the Marketplace Integrity rule, are sharpening the morbidity selection carriers are pricing into 2027 rate filings. The absence of a replacement plan after 15 years is why the ACA stays structurally intact even as these dynamics reshape it. The political environment is shaping how each of the four contrasts above unfolds.

Reading the Retreat Plan by Plan

The 2026 retreat reads differently depending on which kind of health plan you're looking at. Each kind is telling a different operational story about what changed since the 2017 shakeout. The headlines compress them into one narrative (which they shouldn’t), as each tier of retreat is producing a specific signal about which plan operating models are viable in this version of the market and which aren’t.

At the national tier, two of the largest commercial insurers exited within twelve months of each other. The vertical integration math (which I covered in detail in my recent article on Cigna’s exit) is the signal. The Aetna and Cigna exits were capital-allocation decisions, evaluated against the returns those parents could earn by deploying the same capital and management bandwidth into CVS/Caremark and Evernorth/Express Scripts. Sure, the underwriting math contributed, but it didn't drive the call. The 2017 national exits were actuarial. The 2026 national exits are strategic-financial. That’s a different signal, and any plan with deep vertical integration is now evaluating ACA participation against the same internal benchmark.

At the provider-sponsored tier, Baylor Scott & White Health Plan announced in April 2026 it would exit Texas Medicaid by August and stop offering individual marketplace plans after 2026, affecting roughly 100,000 marketplace enrollees and 125,000 Medicaid members. This is the second ACA exit by a Baylor-affiliated plan in the past 9 years. CEO Pete McCanna identified the operating-model problem: high turnover in marketplace and Medicaid populations makes the integrated provider system model harder to sustain than in Medicare Advantage and direct-to-employer populations. A month earlier, Providence Health Plan, the insurance arm of a 51-hospital Catholic health system that sells individual ACA coverage in Oregon and Washington, announced it is exploring strategic options, including a sale. The signal at this tier is that the integrated delivery system model (which is supposed to have a built-in advantage in coordinating care for a defined population) doesn’t have a structural advantage in markets where the population turns over annually, and price elasticity dominates the purchase decision. Provider-sponsored plans pulled back in 2017 too. The 2026 version of the same retreat reinforces that lesson rather than refuting it.

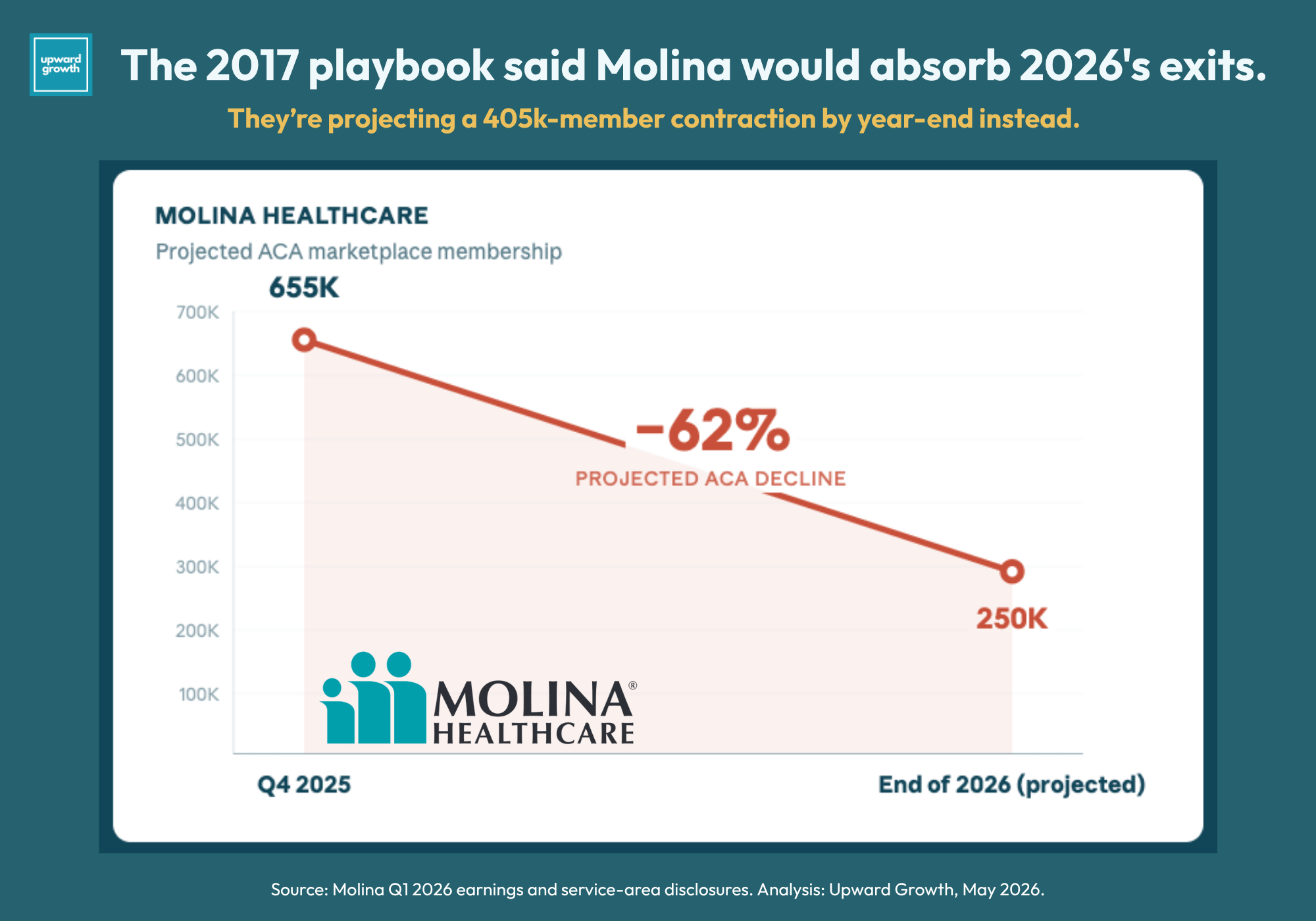

At the Medicaid-DNA tier, Molina Healthcare announced significant 2026 service-area reductions, exiting Michigan and Wisconsin entirely and withdrawing from roughly one-fifth of its counties across eight additional states. Molina projects ACA membership dropping from approximately 655,000 to 250,000 by the end of 2026, a 62% decline. The stock fell 27% hearing the news. Molina is also planning to exit traditional Medicare Advantage in 2027.

Medicaid-DNA pullback isn’t itself new (Ambetter exited Wisconsin and WellCare left Kentucky and New York in 2017), but the scale of Molina’s retrenchment is without 2017 precedent. The signal here is perhaps the most important of the three because it complicates the durability thesis that emerged from the 2017 shakeout. Medicaid-DNA operating models were supposed to be the most durable under the ACA. Molina’s retreat shows that durability is conditional, not categorical: Medicaid-DNA plans win when they have geographic concentration in their existing Medicaid markets, and they lose when they overextend into ACA-only territory in pursuit of growth.

Regional plan turnover (HAP CareSource, Health Alliance, Chorus Community Health Plan, Mountain Health CO-OP exiting Wyoming only, Primewell, UM Health Plan, Celtic/WellCare from North Carolina, BCBS Arizona’s PPO terminations) follows the same pattern the 2017 cycle produced. Michigan’s exchange went from ten participating insurers in 2025 to seven in 2026. What’s different in 2026 is the absorbing cohort. In 2017, the plans absorbing displaced membership were broad: Medicaid-DNA operators leaning in, Blues stepping up, and regional plans growing into vacated counties. In 2026, the absorbing cohort is narrower because Molina is retrenching at scale, and the Medicaid-DNA category is being more selective about where it adds membership. That narrowing of the absorption side is the operational point that should matter most to anyone modeling where displaced ACA members are going to land.

Reading the Plans That Stayed: Five Strategic Postures

Plans operating in the 2026 ACA market can be segmented in several ways: by parent size, by enrollment, by Medicaid managed care exposure, and by geographic concentration. The five postures below are organized by buyer behavior, capital allocation logic, and forward strategic posture because these dimensions predict what each plan does next. If you're triaging a pipeline, rereading a portco, or reframing client work, what a plan does next is what drives your decisions.

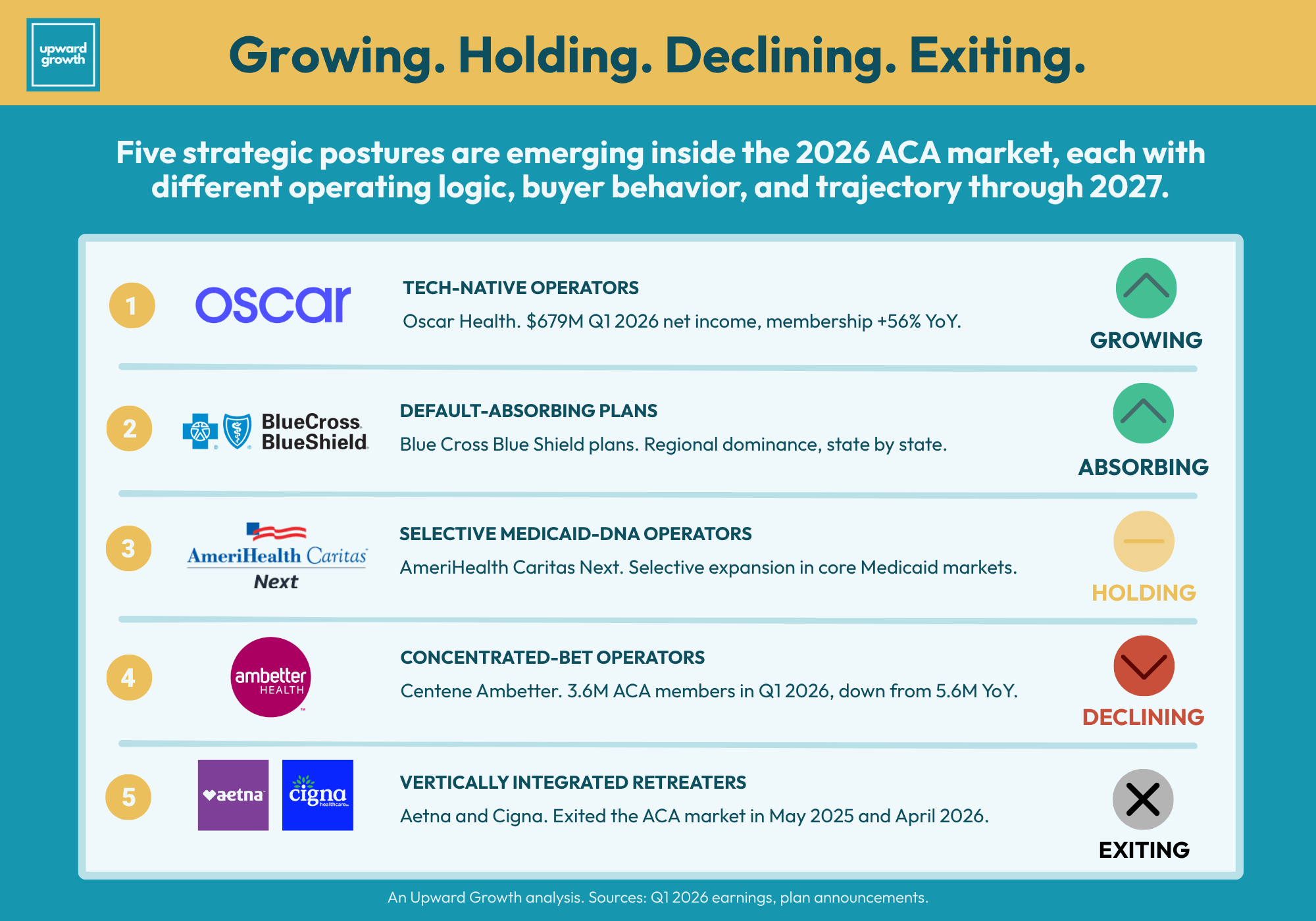

Tech-native operators. Oscar Health turned its first full year of profitability into 56% membership growth. The company was built around technology-enabled member engagement, transparent member experience, and a willingness to operate in individual markets where traditional insurers couldn’t make the economics work. Q1 2026 numbers came in at a record $679 million net income on $4.65 billion in revenue, with medical loss ratio dropping from 75.4% to 70.5%. Management reaffirmed full-year guidance. The buyer this profile produces is one that funds technology investments against measurable return on medical loss ratio, member acquisition cost, or retention, and disengages from vendor pitches that can’t connect to one of those metrics.

Default-absorbing plans. Blue Cross Blue Shield (BCBS) plans hold the dominant ACA position in most state markets. They were there before the nationals arrived, they stayed when nationals walked, and they absorb displaced membership when others exit. Capital allocation logic is mission-adjacent for most BCBS plans, which are nonprofit or operate under community-coverage mandates. In states where the local Blue is the default ACA insurer, vendor and partner go-to-market runs through that plan. The Blues consolidation dynamics I covered earlier are accelerating that reality, because the Blue you’re selling into in 2026 may be operating under a parent organization that controls procurement, contract architecture, and technology standards across multiple states.

Selective Medicaid-DNA operators. AmeriHealth Caritas Next grew its 2026 ACA footprint while Molina cut its own by 62%. AmeriHealth Caritas operates Medicaid managed care plans across multiple states and entered the ACA exchange in 2021, with its Next product expanding into Delaware, Florida, South Carolina, and additional North Carolina counties in 2023 and growing again for 2026. The operating logic mirrors Centene’s at a smaller scale: government-program operating DNA, cost discipline, and a member population overlapping the Medicaid book the plan already serves. The contrast with Molina is in geographic discipline. AmeriHealth Caritas Next expanded ACA only where its existing Medicaid operations provided a cost-of-care anchor. Molina’s ACA footprint outpaced that anchor in several states, which perhaps made the retrenchment necessary.

Concentrated-bet operators. Centene's Ambetter is the clearest example at scale. The company built its commercial story around the ACA Marketplace, and Ambetter is one of the largest individual exchange players by enrollment. ACA membership came in at 3.6 million in Q1 2026, down from 5.6 million a year earlier, a 36% drop. Over one-third of remaining members now hold bronze plans, and 75% of silver membership came from renewals. Two million members lost in a year and still the largest plan in the market. That's what concentrated-bet looks like in 2026: a leading position that's smaller than it was, in a market that's smaller than it was. Vendors and partners selling into Ambetter should expect a buyer sophisticated about ACA-specific economics, disciplined about cost-of-care, and managing a materially smaller book than twelve months ago.

Vertically integrated retreaters. Aetna and Cigna made their decisions 12 months apart, and both were capital-allocation decisions measured against the vertically integrated parts of their respective parent companies. Aetna had losses to point to, including a $448 million premium deficiency reserve in Q1 2025. A price transparency analysis published in early 2026 revealed a structural detail behind those losses: Aetna's ACA exchange networks expanded substantially in 2025 while peer national payers maintained or compressed their exchange networks. Network expansion, higher contracted rates, and a price-sensitive enrollee population drove the cost trend that led to the exit. Anyone modeling the next round of payer ACA exits should weigh network expansion data first. Cigna's exit came from the opposite direction: a smaller ACA book that an incoming actuary CEO determined wasn't worth the management bandwidth relative to Evernorth/Express Scripts. Vendors and partners selling into vertically integrated plans need to make their pitch against that internal capital allocation benchmark, not against ACA-segment economics in isolation.

The key takeaway is that treating the ACA market as a single Total Addressable Market (TAM) was always a stretch, and in 2026, it stops working entirely. Each of the five postures buys differently, funds differently, and operates differently. The work for the rest of this year is figuring out which postures show up in your pipeline, your portfolio, or your client list, and what each one needs from you next.

How To Operate Inside The Shakeout

Here’s how to use the five-postures map. Centene Ambetter, AmeriHealth Caritas Next, a regional Blue, and Oscar each buy on different motions, success metrics, procurement timelines, and willingness-to-pay. A pitch that worked across the ACA-exposed plan list eighteen months ago will land unevenly in 2026, because the plan list itself has changed, and the plans still in the market are operating under a different logic than they were.

Pipeline triage is the next move, and the work is sorting your ACA-exposed deals into three groups. The first group covers plans that have exited or are in significant retreat, including Aetna and Cigna fully, Molina at the service-area level, and a cohort of smaller regional exits. Those deals need to either wind down or be transferred to a surviving line of business within the parent company. The second group is deals at plans still in the market under one of the four staying-in postures. Those deals stay in pipeline, but the posture and buyer may have changed. Reread each one against the posture before your next pipeline call. And the third group is the trickiest: deals where the ACA component is part of a broader plan-wide contract. The contract math at the rollup level might still look fine while the ACA-specific portion has shifted underneath it. Pull the ACA component out and evaluate it on its own merits.

Investor implications cut sharper than the headline numbers suggest. Private equity (PE) and venture capital (VC) firms holding portfolio companies (portcos) with ACA-exposed pipeline need to recalibrate. The TAM math has shifted, the buyer set has narrowed, and the comp set for ACA-focused operators (Oscar as a public comp, the Bright Health post-mortem as a cautionary comp, Centene Ambetter as the scaled comp) is sharper than 18 months ago. Limited partners (LPs) are going to ask.

Provider organization implications are immediate and extend beyond bronze migration. The 2024 risk pool isn’t the 2026 risk pool, and the reason runs deeper than plan tier mix. In 2026 rate filings reviewed by Georgetown’s Center on Health Insurance Reforms, carriers across markets explicitly priced for adverse morbidity selection: healthy enrollees dropping coverage at materially higher rates than sicker enrollees, with Vermont’s MVP assuming healthy subsidized enrollees will drop at twice the rate of other subsidized enrollees, and Maryland’s Optimum Choice and Texas’s Celtic Insurance (Ambetter) both citing the Marketplace Integrity rule as expected to accelerate that healthy-enrollee attrition through eligibility friction. Wakely's modeling projects that if H.R. 1 provisions and the Integrity rule stay in place without ePTC restoration, individual market enrollment could decline 47-57% nationally with deeper losses in non-expansion states. The population that 2024 value-based care actuarial models were built around is turning into a smaller, sicker, more administratively burdened cohort in real time. Renegotiating capitation, shared savings, and downside-risk arrangements is easier now against carriers already pricing for morbidity selection than it will be a year from now after the first cycle of contract underperformance. That actuarial recut is worth starting now.

Management consultancy implications are about giving clients a frame that holds. Clients asking “what does my GTM look like for the ACA market in 2026 and 2027” need a defensible analytical structure to anchor the answer. Use the postures map to segment a client’s addressable plan list and build differentiated GTM motions per posture, so the strategy fits the buyer instead of generalizing across the plan list.

Health plan competitive intelligence (CI) implications run through the membership data. Membership redistribution from Aetna and Cigna exits is concentrating in concentrated-bet, selective Medicaid-DNA, default-absorbing, and tech-native plans. Tracking where displaced members are landing tells CI teams where vendor and partner opportunities are heading next. Plans absorbing membership are also revealing pricing posture in their 2027 rate filings.

What I’m Watching For Through Q3 And Q4

Six indicators on my watchlist heading into the back half of 2026. The 2017 cycle taught me what signals to track when a market sorts itself, and the 2026 differences taught me which of those signals to read differently this time around.

2027 rate filings will soon be landing with state regulators and will be widely available across most states by mid-summer. The question is whether plans staying in are pricing for stable participation or pricing for managed decline. Rate filings show the answer faster than press releases do.

Q2 and Q3 earnings calls from public plans will include ACA-specific commentary worth tracking closely. Molina’s calls matter for a different reason than the others: following the 27% stock drop and the projected 62% decline in ACA membership, those calls will reveal whether Molina is positioning for a complete ACA exit by 2027 or a stabilized, smaller footprint. Centene’s calls will reveal whether the decline from 5.6 million to 3.6 million members has stabilized. The ACA-specific commentary in last week’s earnings synthesis already foreshadowed some of these dynamics. Subscribe to the newsletter to get the Q2 and Q3 syntheses as they land.

The Aetna 2026 absorption pattern is the leading indicator of what the Cigna 2027 picture will look like: which plans absorbed displaced Aetna members, how that changed their enrollee mix and risk pools, and whether the plans that picked up share-priced for it or got caught short. That data lands through Q3 and Q4 2026, right as Cigna’s 2027 wind-down begins. Build the watchlist now.

Congressional movement on ePTC restoration is where I’m putting the most analytical weight, and where the conventional read is most likely to be wrong. The default assumption is that restoration would be a clean positive for the market: healthier enrollees come back, premiums stabilize, bronze migration slows, the shakeout settles. The actual dynamics are more complicated. Restoration this late in the year (or in 2027) wouldn’t undo the structural changes the 2025-2026 cliff already produced. Plans that exited won’t reenter for at least one cycle. Plans that retrenched won’t expand back into the counties they pulled out of based on a single policy signal. The morbidity selection that carriers are pricing into 2026 and 2027 rate filings doesn’t reverse because subsidies return. Restoration would slow the narrowing of absorption capacity I described earlier, which is the more important second-order effect. Continued absence accelerates the shakeout and makes Molina-style retrenchments more likely at other Medicaid-DNA operators. My read for the year-end legislative package: the political path to restoration is narrower than the consensus expects, because Republican leadership has limited incentive to spend capital on ePTC restoration absent a clear electoral threat. The operational read should be biased toward planning for continued absence.

Open enrollment for 2027 starts November 1, 2026. The number that will matter most is whether enrollment stabilizes around the new lower baseline (around 23 million) or continues to decline.

Further plan announcements for 2028 are the last item on the watchlist. The 2026 retreat spans every category of operator, just as the 2017 cycle did. What’s worth watching is whether the cohort of plans absorbing displaced membership is large enough to stabilize the market or whether the absorption capacity is materially thinner than it was in 2018.

Final Thought

The lesson from 2017 that I keep coming back to is that the operators who emerged stronger were the interpreters, not the predictors. They read each retreat in real time as evidence about which operating models would survive a smaller, sicker, more price-sensitive market, and they rebuilt accordingly. Some plans in 2017 were priced and staffed for an enrollment recovery that didn't materialize on the timeline they needed.

The 2026 ACA market won't be a milder version of what came before. It will be a different market: narrower absorption capacity, structurally smaller risk pool, sharper morbidity selection, and a tighter set of buyer postures across the plans that stay. A correct read in 2026 shows up in 2027 as deals closed, portcos repositioned before LP questions get pointed, client frameworks that hold up in plan boardrooms, and risk contracts renegotiated before the first cycle of underperformance.

That reading is the work in front of you right now. It’s also the work we do at Upward Growth. If you want help applying any of the analyses above to your pipeline, portfolio, or client list, please reach out.

The weekly Upward Growth newsletter gives health tech vendors, investors, provider organizations, and management consultancies a clearer view of how the payor market actually works.

If your colleagues are making decisions in this market, they should be reading this too.

💰 Invest in your team with a paid subscription.

💡 Pro tip: Many subscribers expense Upward Growth through their company’s professional development, training, or learning budget. Here’s a one-minute email template to get your manager to approve expensing your subscription.

Week after week you deliver! Appreciate your analysis. Cheers