Q1 2026 Payor Earnings Just Decided What CY 2027 Will Look Like

Five publicly traded payors just signaled how they will price, build, and rationalize for the next cycle. Here's what it means before bid filings lock in June.

Upward Growth provides health tech leaders with the playbooks and proof to transform complex markets into real growth. Each week, we deliver clear, practical strategies on positioning, messaging, and growth, so leaders can close enterprise deals and build repeatable momentum.

🤝 Work with Ryan on payor growth strategy: Contact me

🟦 Connect with the author, Ryan Peterson, on LinkedIn.

📰 Newsletter sponsorships are available: Learn More

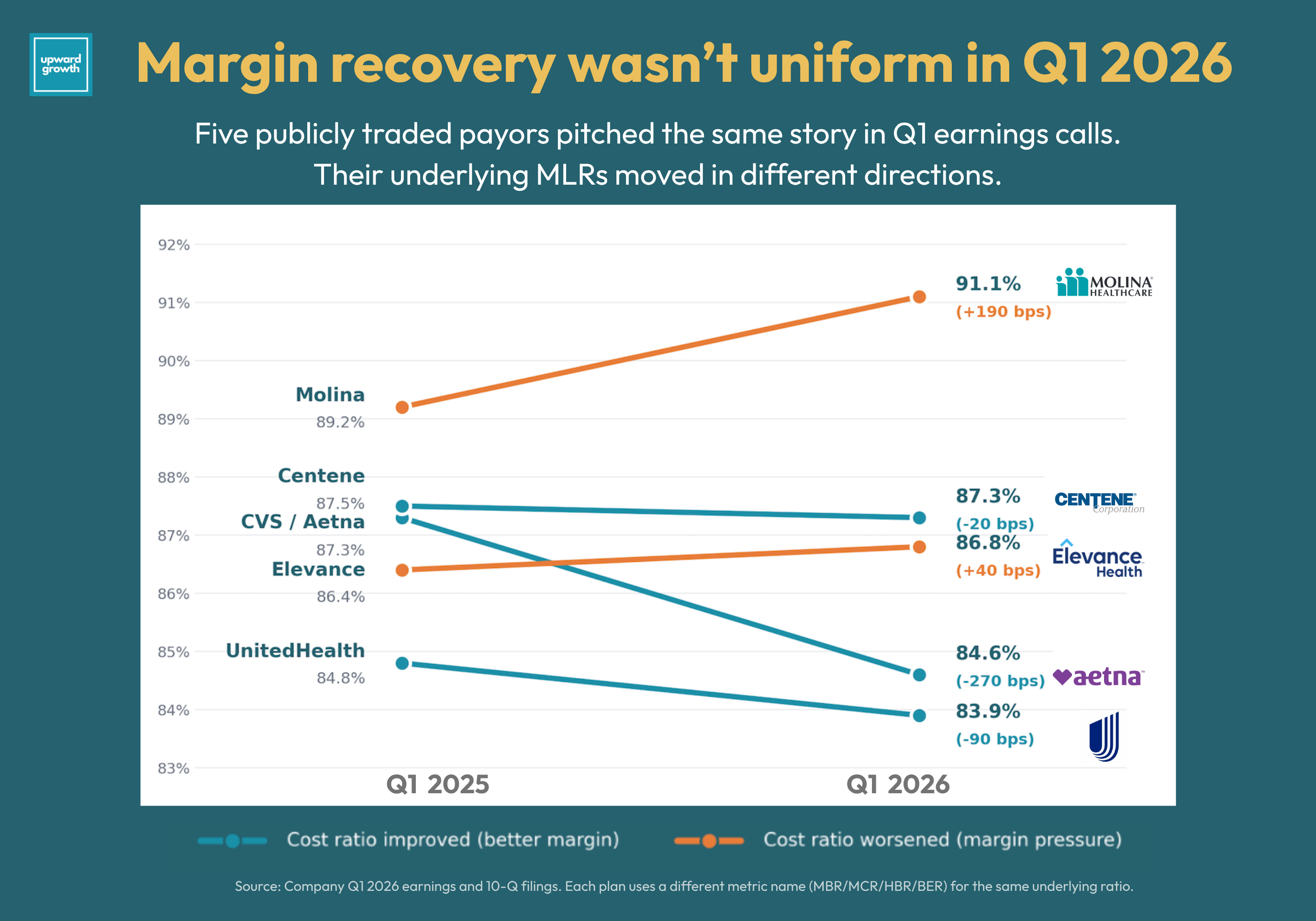

Five publicly traded payors just reported Q1 2026 earnings, and the cross-plan story everyone is writing is “margin over membership.” UnitedHealth on April 21. Elevance on April 22. Molina on April 23. Centene on April 28. CVS on May 6. All five chose to defend margin trajectory rather than chase enrollment growth.

Sure, that was the clear theme that emerged, but the more useful read is what these earnings calls signal about the next six months. Calendar Year (CY) 2027 bids are due to the Centers for Medicare & Medicaid Services (CMS) in early June, with final benefit decisions locked in July and August. Meanwhile, compliance teams are running the audit pass triggered by the Elevance accrual across the industry. By the time the 2027 plan year benefit information becomes public in October, every phrase a CFO used on these calls is already set in stone inside the plan.

This article focuses on UnitedHealth, Elevance, Molina, Centene, and CVS, with Humana and Cigna referenced where their commentary adds to the pattern. A number of readers have asked for the Upward Growth lens on payor earnings calls, so this is the first in a recurring quarterly read of the publicly traded health plans.

What follows is a read on the language and events that did real work this quarter, what got talked about less, and what those signals tell us about where the industry is heading.

What “Disciplined Pricing” Tells You About the CY 2027 Bid Cycle

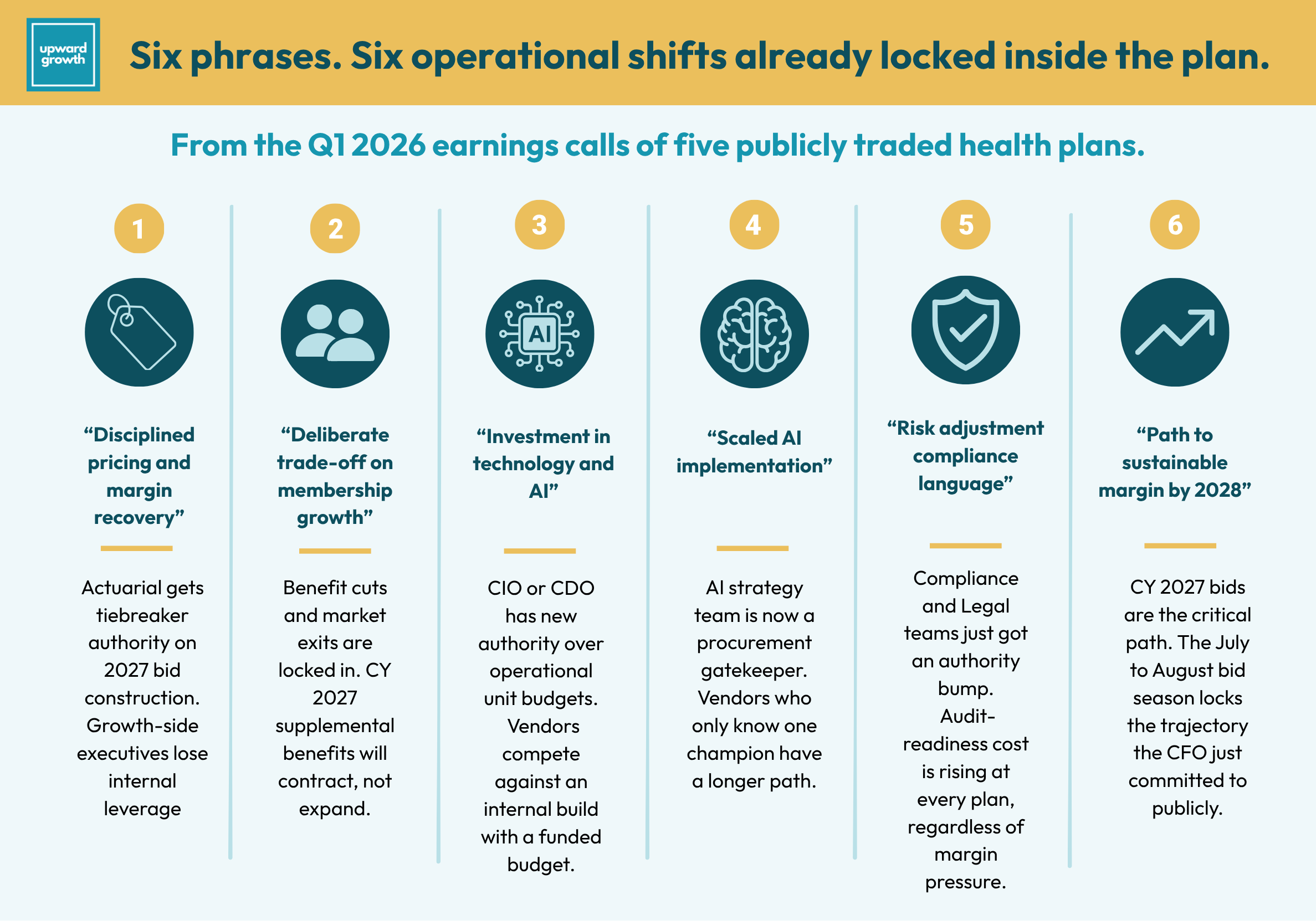

The disciplined pricing language was the most universal across the quarter and anchored everything else these calls said. It tells you how plans will behave heading into the CY 2027 bid window and how aggressive they will be with benefit redesign and product rationalization in late summer.

Stephen Hemsley framed UnitedHealth’s 2026 strategy as margin recovery and product stability with a deliberate trade-off on membership growth. Gail Boudreaux described Elevance as remaining disciplined heading into 2027 bids. Sarah London returned to tangible progress in margin recovery multiple times on Centene’s call. Joe Zubretsky framed the Medicare Advantage Prescription Drug (MAPD) product exit as a discipline move. Steve Nelson at CVS tied disciplined pricing to Aetna’s roughly $1 billion year-over-year operating income improvement. Humana, on its own call, named the 3% sustainable margin by 2028 as Priority One, basically the same frame stated more bluntly. The Cigna leadership transition puts the same trend in the CEO seat: an actuary now runs the company, and the margin discipline message is being institutionalized at the executive level.

Five plans, one frame. Inside the plans themselves, that kind of public commitment usually produces a specific operational sequence. The actuarial team takes the lead role on bid construction. Bids submitted to CMS in early June, benefit decisions lock in July and August, and plans are communicated to brokers in September. By October, the 2027 benefit landscape will become public.

Looking ahead, the bid season we are about to watch will look more like a contraction cycle than a competitive one. The CY 2027 Final Rate Announcement was friendlier than the January preliminary notice, but the gap between funding and trend is still meaningful, and the risk model freeze that made the 2.48% possible is temporary. Plans heard "you have one more cycle" from CMS, and they are using it to defend margin rather than expand benefits. CY 2027 will reflect that.

The internal piece of this is worth flagging. The executive team that said “disciplined” in April cannot walk into a bid review in July and approve a generous benefit redesign without contradicting itself in front of investors. Public language on an earnings call constrains internal decisions over the next four months. That is true at every plan, every quarter, but it matters more in a cycle where the public commitment is to discipline.

The Internal Build Is the Dominant Procurement Story of 2026

The technology and AI investment language on these calls signals where the procurement budget is moving and which categories are getting harder to sell into. Every one of the five plans named it as a 2026 P&L line item, not a future bet.

UnitedHealth committed to roughly $1.5 billion in AI investment for 2026, with about a third concentrated at OptumInsight. Elevance described scaled AI implementation across clinical, operational, and administrative workflows. Aetna’s prepared remarks reported standardizing data requirements for 88% of prior authorization volume, approving 95% of eligible Prior Authorizations (PAs) within 24 hours, processing 83% in real time, and eliminating more than 1 million provider calls through automation. Centene framed cost trend management as process modernization. Molina, the smallest of the five, tied operational efficiency through technology to its embedded earnings story.

A few years ago, the technology language on payor calls was about partnerships and ecosystems. The 2026 language is about internal capability and AI investment. Both words are doing real work. “Internal” means the work is being built or absorbed inside the plan rather than purchased from vendors. “AI” means the productivity assumptions baked into 2026 and 2027 operating budgets already count automation that may or may not actually perform as projected.

Why Vendors Are Losing Health Plan Deals to the Plan’s Own Internal Build covered this dynamic, and the Q1 calls confirm what was already taking shape. No-code and low-code AI tooling has lowered the technical barrier to building functional solutions internally. Health plan CEOs at public companies are under board-level pressure to demonstrate AI leadership, and less to select vendors. Internal builds become assets the plan owns rather than subscriptions it pays for, and that distinction matters to investors and acquirers evaluating long-term enterprise value.

The forward read is that the next two procurement cycles at these plans will favor vendors solving problems the plan cannot credibly build internally, and will be muted toward vendors whose work overlaps with what the plan thinks it can build. The line between those two camps is being redrawn this year, and where it lands determines which vendor categories will be funded in 2027 and which won’t.

The procurement implications run deeper than the budget line. When AI becomes an enterprise commitment, the CIO or CDO has authority that used to live with the operating units. The director of utilization management (UM), who used to make the call on a UM vendor, now has to align with the AI strategy team before signing any new contracts. That changes the procurement path for every category that touches a workflow.

What the $935 Million Elevance Accrual Tells You About the Next Six Months

The Elevance risk adjustment story tells you the most about the next six months, because it is the one story most plans went out of their way not to discuss. Elevance had to address it because of a CMS notice. The other plans had a choice, and most chose silence.

Elevance accrued $935 million on its Q1 financials related to a CMS notice from February 27 about historical Medicare Advantage risk adjustment data submission. The exposure range is wide, with current management estimates putting the possible liability between roughly $350 million and $1.5 billion. The CMS deadline has been extended to July 31, 2026. Boudreaux framed the matter as a historical interpretation dispute and emphasized that current practices and governance are sound.

What stands out is not what Elevance said about it, but what the other plans did not say.

UnitedHealth, Centene, Molina, and CVS were notably careful in their language about risk adjustment, in some cases not addressing it as a discrete topic at all. That is unusual for a quarter when the largest single regulatory action against a national plan in several years happened in that exact space. The silence reads as a choice. Every plan in the country knows its own historical risk adjustment data submission practices are getting reviewed inside its walls right now. Saying that out loud on an earnings call would invite questions about their own exposure that nobody is positioned to answer with confidence.

What this signals for the next six months is that risk adjustment compliance and accuracy are the most consequential industry-wide stories, and almost nobody is writing about it that way. The July 31 CMS deadline sits right in the middle of the bid construction window. Compliance teams at every plan are racing to validate their own historical submissions before regulators come asking. Vendors with offerings in audit, accuracy, and submission process integrity are in the strongest demand environment they have seen in years, even as the rest of the vendor market is feeling margin pressure. That divergence is the part of the story that the financial coverage misses entirely.

The internal authority shift across the plans just gave Compliance and Legal teams a meaningful authority bump. And while risk adjustment operations teams are under their own internal audit, we may now see additional compliance overlay on top of coding accuracy and coding submissions teams.

What These Q1 Payor Earnings Calls Talked About Less

The hardest read on these calls is not decoding what was said but noticing what got dropped. Quarter-over-quarter language comparison is the key here. Three things were notably less present on the Q1 2026 calls than they were on the same five companies’ Q4 2025 calls, and each of the three signals something specific about where the industry is heading.

Supplemental benefit innovation language is mostly gone. The 2025 calls had detailed commentary on Over-the-Counter (OTC) card programs, food-as-medicine pilots, transportation expansion, and various MA supplemental benefit experiments. The 2026 Q1 calls have replaced that language with benefit redesign, market exits, and discipline. CMS rule changes to supplemental benefits, combined with margin pressure, have made benefit expansion a topic that plans are no longer discussing on calls. The signal for CY 2027 is that supplemental benefits will be smaller, simpler, and more rationalized than CY 2026. Plans built around supplemental benefit administration as a primary value proposition should expect contraction, not growth.

Named vendor partnerships have thinned out. The 2024 and 2025 language on these calls often included specific vendor or partner names as proof of innovation. The 2026 calls speak in platform language, internal capability language, and AI investment language. Specific vendor partnerships are visibly less prominent. Whether that is just Investor Relations (IR) script discipline or a real shift in how plans want to talk about vendors publicly is the open question. Either way, the optics of being a named partner have changed. Public co-marketing has historically been a piece of vendor narrative leverage. That leverage is less prominent than it was eighteen months ago.

Growth-specific commentary has been replaced by margin-specific commentary. The headlines capture this, but the magnitude of the shift matters. The 2024 calls had detailed commentary on enrollment growth, market share, and competitive positioning. The 2026 calls have replaced almost all of that with margin trajectory and product stability. Growth language is now framed as a deliberate trade-off rather than a goal. That is a complete reframing of the strategic narrative in roughly eighteen months, and it changes what counts as a credible vendor pitch about anything growth-adjacent.

A dropped talking point is rarely accidental on a public earnings call. Somebody often intentionally decides to drop it, and the reason matters. Tracking what gets de-emphasized across quarters is its own form of market intelligence, and these three drops are worth watching as the year unfolds.

Where the Industry Is Heading Before the Next Cycle Resets

Pulling the threads together, the Q1 2026 calls signal four things about where the industry is heading over the next six to twelve months:

The CY 2027 cycle is a contraction cycle. The disciplined pricing language is a public commitment to a bid season that favors margin defense over benefit expansion. CY 2027 will look noticeably leaner than CY 2026 by the time the benefit landscape becomes public in October. That is the cycle vendors, investors, and consultants need to be planning against right now, before bid filings lock in early June.

The line between vendor categories is being redrawn this year, not next. The internal-build dynamic is not a 2027 procurement story, but a 2026 story already in motion. The areas that will get funded for CY 2027 implementation are being decided in the next few months, and the plans are using the technology investment line to fund internal alternatives that compete with categories vendors used to own.

The Stars story has split into two industries. The plans that have stabilized their Stars investment and those that are still rebuilding from a 2025 hit are now running on different calendars. Aetna explicitly carries leading Stars into 2027. UnitedHealth and Elevance are stable. Humana is openly rebuilding after losing its 2025 Stars lawsuit in October. Centene and Molina were less direct on Stars than in prior quarters. The variance tells Stars vendors which accounts will fund them through Q3 and Q4 and which are still in a defensive posture. The late-summer Stars consolidation (which happens annually) will look meaningfully different in plans that have stabilized than in plans that are still reactive.

The compliance authority shift will outlast the news cycle on Elevance. The Elevance accrual will fade from headlines in a few weeks, but Compliance and Legal teams at every plan now sit atop decisions that used to belong solely to operating units. Meanwhile, procurement paths that ran through quality and risk adjustment operations are may now run through or be augmented by compliance. And that changes the buyer map for any vendor category that touches risk adjustment, quality, or member-level data.

Final Thought

Q1 earnings are the first major data point of the year, and the operational sequence sketched out above runs through August, when CY 2027 bid filings lock in every word these CFOs said in April. By the time Q2 earnings report in late July, Compliance teams will have completed the audit pass that the Elevance accrual triggered, supplemental benefit decisions will be set, and the bid landscape for next year will be public. The next CMS Advance Notice for CY 2028 lands in early 2027, which is when the risk model freeze begins to lift.

The mood on these calls was steadier than it was a year ago. The math underneath the mood has not changed as much as the mood suggests, and the next regulatory cycle is closer than it feels. The plans heard “you have one more cycle” and are using it accordingly. Q2 will tell us whether the discipline holds.

If you are working through what this means for your positioning, your messaging, or your go-to-market strategy, Upward Growth is a health plan market advisory firm that works with health tech vendors, investors, provider organizations, and management consultancies to build strategy around how health plans actually buy, operate, and make decisions. Contact us here.

The weekly Upward Growth newsletter gives health tech vendors, investors, provider organizations, and management consultancies a clearer view of how the payor market actually works.

If your colleagues are making decisions in this market, they should be reading this too.

💰 Invest in your team with a paid subscription.

💡 Pro tip: Many subscribers expense Upward Growth through their company’s professional development, training, or learning budget. Here’s a one-minute email template to get your manager to approve expensing your subscription.