The CY 2027 Final Rule Is Out. What Changed, What's New, and Why It Matters If You Sell to Health Plans.

CMS finalized the biggest Stars overhaul in a decade, rolled back four health equity requirements, and added supplemental benefit rules that weren't even in the proposed rule.

Upward Growth is a health plan market advisory firm. Our weekly newsletter covers payor market strategy, regulatory shifts, and go-to-market insights for health tech vendors, investors, provider organizations, and consultancies competing in the health plan market.

🤝 Work with us on payor market strategy: Contact me

🟦 Connect with the author, Ryan Peterson, on LinkedIn.

📰 Newsletter sponsorships: Learn More

🎁 Unlocked: This post includes the full deep dive

Most Tuesday articles start with a free section and then continue behind the paywall. Today’s post is left completely open so you can read the entire edition.

Paid subscribers get the full deep dive every week, plus playbooks, case breakdowns, and the ability to reply with their own questions.

Q1 is in the books, spring is here, and welcome to that stretch of the regulatory calendar where the final rule and final rate announcement land in the same week, giving everyone who touches the payor market something to stress about. To that end, CMS dropped the CY 2027 Medicare Advantage and Part D final rule on April 2.

Within hours of its release last Thursday, LinkedIn was full of final rule summaries. Most of them were good, and most of them told you what changed. This article explains why it matters and is written for anyone who sells to health plans, invests in companies that do, advises provider organizations that depend on payor contracts, or helps clients make sense of the payor market. The goal is to give you a point of view you can bring into your next meeting without having read the full document (though I still recommend you do).

When the proposed rule came out in December 2025, I broke down six signals that would change how health plans buy. Now we know which ones held. Most of the proposed rule survived intact, but what changed between proposed and final, and what CMS added that wasn’t in the original document, tells you more about the agency’s direction than what stayed the same.

Two surprises worth flagging upfront. The health equity rollback goes further than anyone expected. CMS didn’t just kill the Health Equity Index (HEI) reward. They eliminated four distinct sets of health equity requirements in a single rule. And CMS finalized supplemental benefit and debit card provisions that came from the CY 2026 proposed rule, not the CY 2027 document, so most vendors who tracked the November release have no idea these are coming.

The throughline from CMS is pretty clear: fewer rules, higher stakes, and a smaller set of requirements they fully intend to back up with enforcement. Let’s get into it.

What Changed Between Proposed and Final (And Why the Delta Matters More Than the Rule Itself)

CMS received over 42,000 comments on the proposed rule. What survived the comment period and what didn’t reveals where CMS has conviction and where it backed down under pressure.

Let’s start with Stars. CMS proposed removing 12 measures and finalized 11. The diabetes care eye exam measure survived after pushback from plans and provider groups who argued it drives meaningful clinical action and still shows variation across contracts. One measure out of twelve doesn’t sound like much, but it tells you something worth paying attention to: CMS listens when the clinical case is specific, evidence-backed, and tied to real outcomes. Vague objections about “administrative burden” didn’t move the needle, but targeted clinical arguments did.

CMS also proposed a “provider termination” Special Enrollment Period (SEP) that would have allowed members to switch plans when their provider left the network, but that provision was not finalized. CMS pulled it back entirely, stating it will consider future rulemaking. Withdrawing one of the bigger proposals in the original document signals caution about disrupting plan stability while plans are already dealing with benefit cuts, market exits, and over 1.8 million members forced to choose new plans.

Here’s the overall pattern: all deregulation provisions finalized, all Inflation Reduction Act (IRA) codification finalized, 11 of 12 Stars measure removals finalized, and every health equity rollback finalized. The Requests for Information (RFIs) on risk adjustment modernization, Chronic Condition Special Needs Plan (C-SNP) dual enrollment, and wellness/nutrition policy didn’t produce rule changes (CMS said it will consider comments for future rulemaking), but the provisions that were on the table moved forward with almost everything intact. CMS had the estimated spending impact from the Stars changes alone modeled at nearly $14 billion in additional Medicare spending over the next decade, and they didn’t blink.

For companies selling into payors, this matters because it shows you where objections work and where they don’t. If you’re trying to make a case to a buyer that a certain capability still matters, your argument needs to look like the eye exam defense (specific, clinical, evidence-backed) rather than the provider termination SEP (broad, structural, politically complicated).

That delta between proposed and final also tells you something about CMS’s broader direction, which becomes clearer when you look at what they did with health equity.

The Health Equity Rollback Is Bigger Than the Headline

Most coverage of this rule will report that CMS killed the HEI reward and leave it at that. That’s the headline, but it’s only one piece of a much larger shift. CMS finalized four distinct health equity rollbacks in a single rule: they eliminated the requirement for MA quality improvement programs to include health disparities reduction activities, removed health equity requirements for MA Utilization Management (UM) committees (including the health equity expert member requirement), killed the annual health equity analysis and its public posting obligation, and rescinded the requirement for plans to send mid-year notices about unused supplemental benefits.

None of these is surprising on its own. Industry observers like Crowell & Moring noted these rollbacks were expected, given the administration’s position on DEI-related requirements. But most vendors are processing them one at a time instead of recognizing what they add up to: the compliance infrastructure that justified an entire category of vendor purchases just got dismantled.

If you sell health equity analytics, social determinants of health (SDOH) solutions, or population health tools, the buying signal just changed. When your pitch relied on “plans are required to do this,” the mandate was doing a lot of the selling for you. That mandate is gone. Plans serving dually eligible populations, plans in markets with significant disparities, and plans competing on quality where outcomes vary widely still need this work. But the conversation shifts from “we have to” to “we choose to,” and “we choose to” requires a much stronger ROI case than a regulatory citation ever did.

If your value proposition still leads with requirements CMS just eliminated, you have a positioning problem to fix before your next buyer call. That means rebuilding around financial outcomes a CFO can defend in a budget meeting: cost avoided per member, gaps closed per quarter, readmission reductions that show up in the medical loss ratio (MLR). The buyers still funding vendors right now are the ones whose CFOs can stress-test the ROI at 70% of projected performance and still see the math work.

One more thing worth noting here: even as CMS rolls back requirements, enforcement hasn’t relaxed. The Office of Inspector General (OIG) released its first MA-specific compliance guidance since 1999 in February 2026, the Department of Justice (DOJ) recovered $6.8 billion through False Claims Act (FCA) cases in FY 2025, and risk adjustment remains a top enforcement priority. Fewer reporting requirements doesn’t mean less exposure, but it does mean plans have fewer internal checkpoints catching problems before a regulator does.

The health equity rollback reshapes who buys and why, but the Stars overhaul reshapes what every plan gets measured on.

11 Measures Removed, One Added. The One They Added Is the One to Watch.

CMS confirmed the removal of 11 measures from the Stars program, mostly administrative and process measures where plans were scoring high with little variation between contracts, and refocused the program on clinical care, outcomes, and member experience where meaningful performance differences actually exist.

To understand the magnitude: CMS estimates these Stars changes will produce a net impact of $18.6 billion on the Medicare Trust Fund from 2027 through 2036 (a separate and larger figure than the $14 billion in additional Medicare spending from the overall policy changes, because the Trust Fund estimate captures the downstream effects on Quality Bonus Payments (QBPs) and plan rebates). Press Ganey’s modeling, which was based on the proposed rule’s 12 measure removals with 11 ultimately finalized, projected $1.3 billion in QBP losses and estimated that roughly a quarter of MA contracts could lose half a Star.

Those administrative measures weren’t just easy points, they were also a buffer. Plans that scored well on them could absorb a weak year on a clinical measure without losing their overall Star rating. Now that some of that buffer is gone, the math gets harder in two ways: the Consumer Assessment of Healthcare Providers and Systems (CAHPS) survey and Health Outcomes Survey (HOS) will account for nearly 40% of total Star weight by 2029, and each remaining measure now carries more relative weight, which means a single bad performance year does more damage than it used to. For plans that treated member experience as a secondary priority behind clinical gap closure, that calculus just flipped.

CMS described this as “fundamentally shifting our approach to quality” and “moving away from administrative box-checking.” Adding a new clinical measure in the same rule that removes 11 administrative ones makes that statement hard to misread.

And that new measure is the sleeper. CMS added Depression Screening and Follow-Up, effective for the 2027 measurement year and reflected in 2029 Star Ratings. Behavioral health vendors now have something they’ve rarely had in Stars conversations: a discrete, measurable quality hook tied to a specific measure with a defined timeline. “We directly impact your Depression Screening and Follow-Up score” is a materially sharper pitch than “we improve behavioral health outcomes,” and it gives the health plan Stars team something concrete to model.

There’s a second financial angle that goes beyond Stars. Better depression screening produces better behavioral health documentation, which flows into risk adjustment. A plan that identifies and documents a previously undiagnosed major depressive disorder isn’t just closing a Stars gap; they’re potentially capturing a Hierarchical Condition Category (HCC) code that improves their risk-adjusted revenue. Behavioral health vendors who can quantify both the Stars impact and the risk adjustment lift have a dual financial hook that most competitors aren’t connecting yet.

For member experience and CAHPS-focused solutions, the relative weight increase means every percentage point of CAHPS improvement now carries more financial weight than it did under the old measure set. And if your value proposition was tied to any of the removed measures, the repositioning window is narrow, since CY 2027 bids are being built right now.

What plans get measured on is only half the story. The next set of provisions covers operational requirements that most vendors tracking the 2027 regulatory cycle haven't even seen yet.

The Supplemental Benefit Rules Nobody Saw Coming

If you followed the CY 2027 proposed rule closely (or read my article covering it), these provisions weren’t in it. CMS finalized two supplemental benefit policies from the CY 2026 proposed rule, and they landed in this final rule without the advance notice that vendors tracking the 2027 regulatory cycle would have expected.

Two provisions, both operational, both worth understanding even if you don’t sell supplemental benefits directly.

First, plans must now publicly post the eligibility criteria they use to determine which chronically ill members qualify for Special Supplemental Benefits for the Chronically Ill (SSBCI). That means the internal criteria that used to live inside the plan’s operations are now visible to competitors, regulators, members, and advocacy groups.

Second, supplemental benefit debit cards must now be electronically linked to plan-covered items through a real-time point-of-sale (POS) verification system that confirms eligibility at the time of purchase, and cards are limited to the specific plan year. No more carrying balances or using cards for items outside the benefit design.

These rules land in a market that’s already under pressure. Roughly 30% of Medicare Advantage Organizations (MAOs) now offer flex cards with at least one nonmedical supplemental benefit, with average annual values reaching $1,430, and the flex card market is still growing. But plans have also been pulling back supplemental benefits broadly: OTC allowances dropped from 73% to 66% of plans, meals from 65% to 57%, and transportation from 30% to 24% between 2025 and 2026. Plans are cutting benefits and being told to tighten controls on the ones that remain, and that squeeze is going to force hard conversations between plans and their supplemental benefit vendors over the next 60 days.

If you sell benefits administration platforms, card technology, or supplemental benefit solutions, the real-time POS verification requirement is a technology mandate, and plans will surface whether your platform supports it during CY 2027 bid preparation. If you're a plan evaluating your current card vendor, this is the question that tells you whether your partner saw this coming or got caught flat-footed.

This SSBCI transparency requirement is part of a broader pattern. Plans were already required to post prior authorization metrics on their public websites as of March 31, including denial rates, turnaround times, and appeals outcomes. Now, SSBCI eligibility criteria join that list. For the first time, regulators, competitors, advocacy groups, and anyone selling into health plans can see how a plan operationalizes its supplemental benefits and how it handles prior auth without ever getting on a call with anyone at the plan.

This is pre-call intelligence that didn’t exist a year ago. You can see a plan’s SSBCI criteria before your first meeting and reference their prior auth metrics in a discovery call. And as I wrote in January when the prior auth deadlines hit, plans that met the deadline by speeding up denials didn’t eliminate friction, they relocated it into appeals, provider relations, and member experience. Now those relocated problems are visible in the public metrics. Plans know this information is out there, which means they’re more receptive to vendors who can help them make those numbers defensible.

CMS tightened controls on supplemental benefits in the same rule where it loosened requirements on nearly everything else, and that tension is the story of this entire rule. It's also where the budget opportunity lives.

The Deregulation Pattern (And Where the Freed-Up Budget Goes)

CMS explicitly cited Executive Order 14192 across multiple provisions in this rule. Health equity requirements, mid-year supplemental benefit notices, UM committee mandates, agent and broker restrictions, call center requirements, and creditable coverage disclosures. All of these rolled back in a single document.

For enrollment and distribution tech companies, the agent and broker changes deserve a closer look. CMS removed the 48-hour Scope of Appointment (SOA) waiting period, allowed marketing events to immediately follow educational events, and removed restrictions on how licensed agents interact with beneficiaries. That opens up the agent sales motion considerably.

But here’s what makes it interesting: plans have been cutting supplemental benefits (things like over-the-counter allowances, meal delivery, transportation to appointments, and the flex cards that pay for them) for two years running. So you have more agents selling more aggressively into thinner benefit packages, which means agents will naturally gravitate toward plans that kept their supplemental benefits, because those plans have something compelling to actually offer. If you help plans with enrollment, distribution, or member acquisition, plans with the strongest remaining benefit packages now have a distribution advantage they didn’t have six months ago, and they need the technology to act on it.

The bigger story in this section is about where the freed-up money goes. Health equity analysis staff, UM committee health equity expert roles, mid-year notice production, annual health equity analysis creation and public posting. All of those activities required budget, people, and vendor support. When plans no longer need to fund them, that budget migrates somewhere. Some gets banked as savings by plans under margin pressure. Some shifts toward areas where CMS is increasing scrutiny, like supplemental benefit compliance and Stars measure performance. If you can connect your solution to where that budget is heading, you have a timing advantage over competitors still pitching into compliance categories that no longer exist.

Here’s the tension that runs through the entire rule: CMS simplified the requirements, but the consequences for getting them wrong haven’t changed. Medicare Advantage fraud remains a top enforcement priority for both DOJ and OIG, and several of the removed Stars measures (timely claims processing, call center responsiveness, enrollment and disenrollment processing) served as built-in operational checkpoints. Plans reported on them because they had to, and in doing so, they caught problems early. With those measures gone, plans lose the internal early warning systems they’ve relied on for years. For compliance, documentation integrity, and audit-readiness vendors, the pitch isn’t “enforcement hasn’t relaxed.” The pitch is “the safety nets your buyer relied on are gone, and they need something to replace them.”

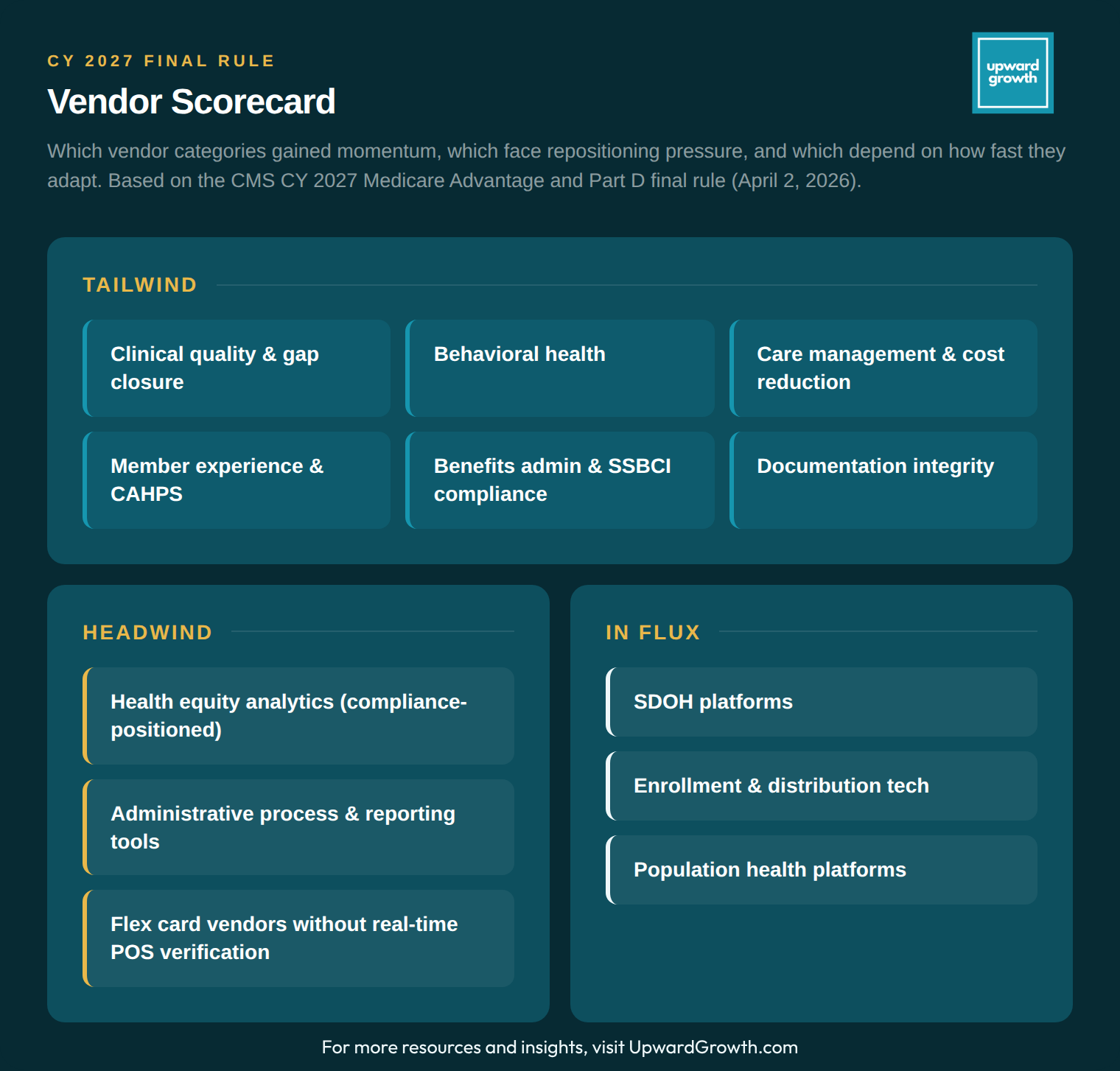

What This Rule Means for Each Vendor Category

The scorecard above maps where each vendor category lands after this rule. But the more useful takeaway isn’t which column you’re in. It’s what the rule tells you about how your buyer’s internal priorities just shifted. Plans that used to spend budget and staff time on health equity reporting, UM committee compliance, and administrative measure tracking now have capacity and dollars that need to go somewhere. The vendors who win CY 2027 deals are the ones who can credibly say “that budget should come to us, and here’s the financial case for why.” If you can’t make that case in language a CFO would defend in a budget meeting, the budget gets banked as savings or goes to a competitor who can.

SDOH, enrollment tech, and population health platforms are the ones to watch here. The mandate is gone, but the operational need remains, and the buyers who still invest will do so because someone made the outcomes and ROI case clearly enough that “we choose to” felt like an obvious decision.

Part D Is Now Permanent. Your Financial Models Should Be Too.

And finally, CMS codified the IRA-driven Part D redesign into permanent regulation, locking in the $2,000 out-of-pocket cap (adjusted to $2,100 for 2026), the elimination of the coverage gap, catastrophic phase changes, and the Manufacturer Discount Program. These changes were already in effect through program instructions, but with that authority expiring, CMS wrote them into the permanent rules, which means plans can stop wondering whether any of this might reverse and instead they can start treating these economics as the baseline for every financial model going forward. If your solution touches pharmacy costs, medication adherence, or Part D plan economics, your ROI projections can now assume these margin pressures are permanent.

Final Thought

Four months ago, I wrote about six signals from the proposed rule and said the theme was uncertainty. CMS has now answered most of those questions, and the answer across nearly every provision was: we meant it.

The direction is consistent enough to build a strategy around: Clinical outcomes over administrative process. Tighter controls where CMS sees abuse, lighter requirements where it sees unnecessary burden. Permanent Part D economics. Enforcement that hasn’t blinked even as the rule set shrinks.

CMS wants fewer rules that matter more, and this rule is the clearest signal yet of what “matters more” actually looks like.

The frameworks in the weekly Upward Growth newsletter help health tech sales and marketing teams navigate payor conversations as the market continues to shift.

If your colleagues are in those conversations, they should be reading this too.

💰 Invest In Your Team with a Paid Subscription.

💡 Pro tip: Many subscribers expense Upward Growth through their company’s professional development, training, or learning budget. Here’s a one-minute email template to get your manager to approve expensing your subscription.