The CY 2027 Rate Announcement Changed Your Buyer's Mood. Here's What That Actually Means for Your Pipeline.

CMS reversed the January rate scare with a $13 billion increase for MA plans. But relief and loose budgets aren't the same thing, and the risk model freeze that made this number possible is temporary.

Upward Growth is a health plan market advisory firm. We work with health tech vendors, investors, provider organizations, and management consultancies to build go-to-market strategy around how health plans actually buy, operate, and make decisions. This weekly newsletter is where we share what we're seeing in the market.

🤝 Work with Ryan on payor growth strategy: Contact me

🟦 Connect with the author, Ryan Peterson, on LinkedIn.

📰 Newsletter sponsorships are available: Learn More

The Centers for Medicare & Medicaid Services (CMS) issued two massive documents to the payor market in the span of five days. On Thursday, April 2, the Final Rule landed, and I covered what it means for selling into payers. Then on Monday, April 6, CMS released the CY 2027 Rate Announcement, and this one deserves its own article because the Final Rule is about policy while the Rate Announcement is about money, and money is what changes how your buyer behaves.

Here’s the headline: CMS is sending $13 billion more to Medicare Advantage (MA) plans in 2027 than in 2026, a 2.48% net average increase that’s a dramatic reversal from the 0.09% CMS proposed in January 2026. When that January number dropped, health insurer stocks cratered. Humana fell over 20%. UnitedHealth lost 19%. Plans started modeling benefit cuts, market exits, and vendor contract reductions. On April 6, the mood flipped: UnitedHealth jumped 11%, Humana climbed 9%, and CVS gained nearly 9%.

The rate bump does not mean stalled deals are about to start moving again, and most vendors I’m hearing from are wrong about the timeline. What follows is a breakdown of what the Rate Announcement actually changes about your health plan buyer’s behavior over the next 12 months, where it creates real urgency to buy, and why the single most important number in this announcement isn’t the 2.48%.

The $13 Billion Swing

In January, CMS proposed a 0.09% rate increase for CY 2027. To put that in context, plans received a 5.06% increase for CY 2026, so the January proposal represented a near-5-point year-over-year drop, the smallest proposed increase in recent memory. CMS estimated it would deliver roughly $700 million in additional MA payments, but compared to the billions in additional funding plans had received in prior years, the number landed as a de facto cut, and the industry sentiment treated it that way.

On April 6, CMS finalized a 2.48% increase, translating to over $13 billion in additional payments and representing a swing of roughly $12 billion between what January proposed and what April delivered.

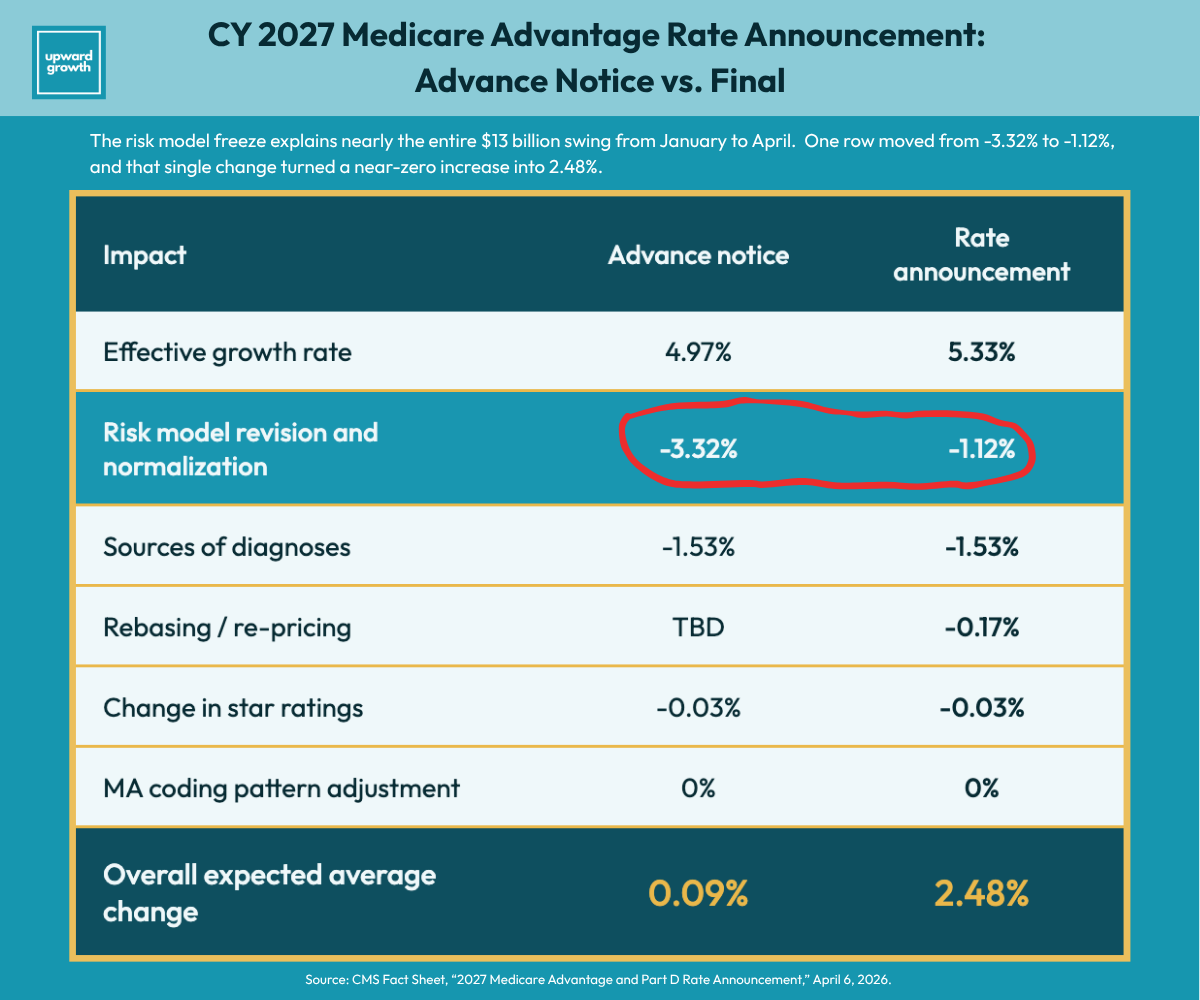

Here’s the CMS table that tells the story:

Look at the Risk Model Revision and Normalization line. It moved from -3.32% to -1.12%, and that single row explains almost the entire $13 billion swing. CMS also updated the effective growth rate from 4.97% to 5.33% after incorporating Q4 2025 fee-for-service cost data, which added real dollars. But even at 2.48%, the increase doesn’t keep pace with the utilization trends plans are reporting: inpatient costs, Part B drugs, post-acute care, and behavioral health are all running hot, and plans heading into bid season know their cost pressures are growing faster than their revenue. The risk model row is where the real story lives, and understanding why it moved tells you more about the next 12 months than the 2.48% headline does.

The Risk Model Freeze Is the Real Story

This is the part of the announcement that matters most, and it requires some context to understand.

CMS uses a risk adjustment (RA) model to determine how much it pays MA plans for each enrolled member. The model assigns a risk score based on the member’s diagnosed conditions, and that score drives the per-member payment. When CMS updates the model, the math behind every plan’s revenue changes.

The current RA model, known as the 2024 model, was built on 2018 diagnosis data and 2019 spending data. It went through a three-year phase-in: one-third of risk scores were calculated under the new model in 2024, two-thirds in 2025, and full implementation arrived in 2026. Plans spent three years absorbing those changes.

In January 2026, CMS proposed replacing this model for CY 2027 with a recalibrated version using 2023 diagnoses and 2024 expenditures. That proposed recalibration was the -3.32% line in the table above, and it was the single biggest reason the January 2026 Advance Notice landed at 0.09%.

CMS pulled the update entirely, so the current model stays in place for CY 2027.

Two things drove this decision. First, the 2024 expenditure data contained a spending anomaly tied to skin substitute products that would have distorted the model’s coefficients, effectively building the new model on flawed inputs. Second, CMS acknowledged that plans had just finished absorbing the V28 RA model phase-in and needed those changes to settle before another recalibration layered on top. On the CMS press call, Director of Medicare Chris Klomp framed it as giving plans time to adjust, while stressing that CMS has not abandoned the recalibration and will keep a “careful eye” on insurer practices.

Here’s why this matters more than the 2.48% headline. The 0.09% that terrified the industry in January 2026 wasn’t a hypothetical. It was the actual rate CMS proposed, including the recalibration. The only reason April 2026’s number landed at 2.48% is because CMS removed the recalibration from the equation. When CMS reintroduces the updated model (and they’ve said they will), the math reverts to something that looks a lot more like the January 2026 Advance Notice. Essentially, the Advance Notice is a preview of the next cycle.

Anyone building a strategy or a pipeline around 2.48% as a new baseline is mispricing what’s ahead. CMS described its vision for risk adjustment in terms of three guiding principles: simplicity, competition regardless of plan size, and payments that accurately reflect beneficiary health risk. That language signals an agency that simply paused, not one that backed down.

For vendors, this changes how you position multi-year contracts. If your deal is structured around a two- or three-year commitment, your buyer is already thinking about what happens when the freeze lifts, and you should be too. The rate announcement shifted plans from surviving the rules to winning the bid, and the vendors who can quantify their value under both the current model and a recalibrated one have a positioning advantage over competitors selling as if the current rate environment is permanent.

The risk model freeze also sets the context for the next big operational change in the Rate Announcement: what CMS did with chart review.

What the Chart Review Exclusion Actually Changed

If you don’t sell risk adjustment tools, you might be tempted to skip this section. Don’t. The chart review exclusion in this Rate Announcement is going to affect your buyer’s financial position, their budget priorities, and the competitive dynamics between the plans you’re selling to, regardless of what you sell. Understanding why starts with how health plan revenue actually works.

MA plans are paid based on the health risk of their enrolled members: the sicker the population, the higher the CMS payment. Plans submit diagnosis codes for each member, CMS converts those codes into a risk score, and the risk score determines the per-member payment. If a member has diabetes, heart failure, and depression, but only diabetes is coded and submitted, the plan gets paid for a diabetic, not for someone with three chronic conditions. Revenue for an MA plan is directly tied to how completely those submissions reflect the actual health of their population.

Chart review is one of the primary ways plans close that gap. A chart review vendor reviews medical records, identifies conditions that were diagnosed but never properly coded or submitted, and sends those additional diagnoses to CMS for risk score calculation. Some of those chart review records are “linked” to a specific clinical encounter, such as an office visit or a procedure, and those records are unaffected by this rule change. Others are “unlinked,” meaning the diagnosis was found in a medical record but can’t be tied to a specific dated encounter. That’s the category CMS just excluded.

For years, CMS allowed unlinked chart review submissions. Plans built significant portions of their risk-adjusted revenue around this practice, particularly through in-home health risk assessments and third-party retrospective chart review vendors. Plans optimized around what was permitted, which is exactly what you’d expect them to do.

Starting in CY 2027, CMS changed the rules: diagnoses from unlinked chart review records no longer count for risk score calculation. If a diagnosis can’t be tied to a documented clinical encounter, it doesn’t affect payment.

According to CMS, 85% of the 88.8 million unlinked chart review records submitted in 2023 for 2024 payment couldn’t be matched to any encounter data record. Average payment impact of the exclusion: -1.24%. CMS carved out an exception for beneficiaries who switch between MA organizations (the “switcher exception”), without which the impact would have been -1.78%.

That -1.24% is an average. The variation across plans is enormous. Plans that built their risk adjustment strategy around unlinked chart reviews are absorbing a much larger hit, while plans that relied primarily on encounter-based documentation are barely affected. An important note on framing: plans didn’t do anything improper here. CMS allowed this practice, plans optimized within the rules, and CMS changed the rules. If you sell to plans, that distinction matters in every conversation you have about this topic.

How the Chart Review Exclusion Hits Every Vendor’s Budget

Here’s why this matters even if you don’t sell risk adjustment tools. When a plan loses meaningful revenue due to the chart review exclusion, that financial pressure doesn’t stay within the risk adjustment department. It shows up in budget decisions across every vendor category. A plan absorbing a -2% or -3% revenue hit is going to scrutinize every line item, including your care management contract, your quality reporting platform, and your member engagement tool.

This creates a paradox worth watching. The same exclusion that pressures some buyers’ budgets also creates emergency-level procurement urgency for others. Plans that lost revenue need to shift from retrospective documentation to prospective risk capture, meaning they need to start documenting diagnoses during actual clinical encounters rather than finding them after the fact in medical records. That shift requires encounter data remediation tools, prospective coding workflow platforms, and better linking between chart review submissions and encounter records.

If you sell in that space, some of your prospects are moving faster than they’ve ever moved. But if the exposure is severe enough at a given plan, the budget cuts from lost revenue could stall your deal before the urgency translates into a purchase order. Which dynamic dominates depends on how exposed your specific buyer is, and that’s a question you need to answer before you forecast.

Also, note this policy is part of a multi-year CMS trajectory to tighten how diagnoses translate into payments, meaning the financial pressure on heavily exposed plans is structural, not a one-time adjustment. That structural pressure shapes how the rate announcement actually hits vendor procurement budgets, and it’s the question most vendors are getting wrong right now.

When the Rate Announcement Actually Shows Up in Your Deal

Sure, the 2.48% improved the mood, but unfortunately, it won't loosen budgets on the timeline most vendors are expecting.

Health plans are heading into bid season right now, with bids due to CMS in June 2026. Those bids determine what each plan offers members in CY 2027: the benefits, the premiums, the provider networks. Vendor budgets for CY 2027 are largely set as part of that process. The rate announcement confirms what plans have to work with, but it doesn’t create new vendor spend for the current cycle. For most vendors, the financial relief from the 2.48% increase won’t show up in procurement budgets until CY 2028. It will improve your buyer’s willingness to start conversations for next year’s implementation, but it won’t accelerate a deal this quarter.

One exception, and it’s specific: vendors selling solutions to problems the Rate Announcement just created. Encounter data remediation, prospective risk capture, and chart review linking. When a plan’s CFO realizes that unlinked chart review diagnoses are being excluded from risk scores starting CY 2027, procurement shifts from “next year’s budget” to “we need this before our next submission window.” Those purchases break the normal budget cycle because they address an immediate revenue protection problem.

For everyone else, patience is the right posture. Internal health plan forces drive deal timing: budget cycles, bid timelines, steering committee approvals, and procurement queues all operate on their own calendar, and a favorable rate announcement doesn’t override those mechanics.

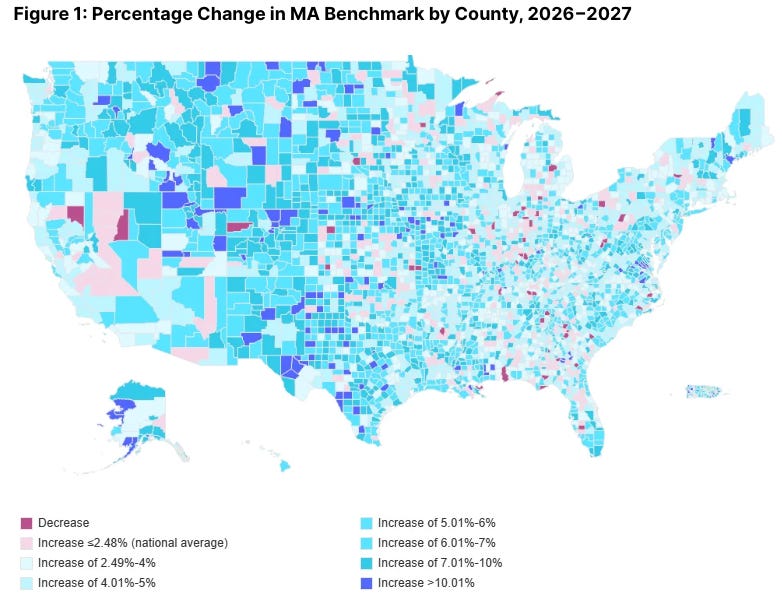

And the 2.48% itself deserves scrutiny at the local level. Health policy research firm Avalere Health published a county-level analysis showing that the national average masks enormous geographic variation, with county-level benchmark changes ranging from -4.5% to +19.8%.

Before your next pipeline review, look at the map above. If your prospects operate primarily in counties that saw decreases or flat benchmarks, the 2.48% headline isn’t their reality, and your deal assumptions need to reflect that. If they’re in counties with above-average increases, the relief is real…but so is the increased competition from other vendors who see the same opening.

For context on how much local variation matters: even in CY 2026, when plans received a 5.06% increase (more than double what they’re getting for CY 2027), nearly 50% of counties saw at least one plan terminate, and in 21 counties every MA plan was terminated.

Your buyer’s emotional state changed, but their budget math may not have changed as much as you think. That’s why, when your buyer brings up the rate announcement, the right response is demonstrating that you understand 2.48% is breathing room in the aggregate and that the math looks different depending on where they operate.

Final Thought

The risk model freeze is the reason the 2.48% landed where it did, and the freeze is temporary. CMS said so on the record.

Health plans are building bids right now with a 12-month window of stability that closes as early as January 2027 when the next Advance Notice drops. Your buyer’s emotional state changed. Their budget math may not have changed as much as you think.

Vendors who use this window to get in front of buyers while the mood is favorable, position around the operational problems the announcement created, and build relationships before the next regulatory cycle resets the board will have pipeline built when the next Advance Notice lands. Vendors who wait for the budget environment to “fully improve” will find themselves starting conversations in late 2027 while everyone else is already in procurement.

If you're working through what this means for your positioning, your messaging, or your go-to-market strategy, Upward Growth is a health plan market advisory firm that works with health tech vendors, investors, provider organizations, and management consultancies to build strategy around how health plans actually buy, operate, and make decisions. Contact us here.

The frameworks in the weekly Upward Growth newsletter help health tech sales and marketing teams navigate payor conversations as the market continues to shift.

If your colleagues are in those conversations, they should be reading this too.

💰 Invest In Your Team with a Paid Subscription.

💡 Pro tip: Many subscribers expense Upward Growth through their company’s professional development, training, or learning budget. Here’s a one-minute email template to get your manager to approve expensing your subscription.